Stablecoins and shenanigans, with Zeke Faux

This week I'm joined by Bloomberg investigative journalist Zeke Faux. He's been the mainstream media's most dogged reporter on the Tether beat, and wrote what I consider the best book yet on cryptocurrency: Number Go Up. (I reviewed it.) In addition to discussing the quilt of red flags, we talk about pending legislation to regulate stablecoin issuance in the U.S., and also the synthesis of investigative journalism by institutions, experts without press badges who still buy e-ink by the barrel, and the Baker's Street Irregulars of cryptoskeptic Twitter.

[Patrick notes: I add notes, set out in this fashion, after recording the episode. As I was writing those notes, while I feel like my prior writing on stablecoins talks about the potential of it, there was an opportunity here to present the bull case—so to speak—in more depth than we did. I got too fascinated by our rollicking conversation and ran out of time. So, docking myself one cookie, and committing to writing something on that at some point in the future.]

Sponsors

Check is the leading payroll infrastructure provider and pioneer of embedded payroll. Check makes it easy for any SaaS platform to build a payroll business, and already powers 60+ popular platforms. Head to checkhq.com/complex and tell them patio11 sent you.

Timestamps

(00:00) Intro

(00:45) The GENIUS act of 2025

(02:28) Tether's audit controversy

(05:49) The origins and impact of Tether

(08:17) Investigative reporting and red flags

(12:58) Tether's shady business practices

(19:23) Tether meets SBF

(21:40) Sponsor: Check

(22:51) New anecdotes in the Number Go Up paperback

(28:53) The role of stable coins in crime

(38:20) The importance of AML and KYC rules

(44:21) Financial privacy

(45:18) Sam Bankman-Fried's conference in the Bahamas

(47:14) Loot NFTs

(49:34) Axie Infinity: a case study

(52:30) Crypto's real-world consequences

(58:15) Regulation and financial safety

(01:05:40) Stablecoin bill and ownership limits

(01:06:50) Political realignment and crypto

(01:14:40) Citizen journalists and the crypto-skeptic community

(01:20:36) The abilities and limitations of institutional journalists

(01:26:00) Wrap

Transcript

Patrick: Hideho, everybody. My name is Patrick McKenzie, better known as patio11 on the internet, and I'm here with my buddy Zeke Faux, who's an investigative journalist at Bloomberg and the author of "Number Go Up."

Zeke: Hey, Patrick.

Patrick: Good to have you here. As I mentioned in my review of it - and I'll link it in the notes - "Number Go Up" is my favorite crypto book, which is appropriate because it's going to be a very crypto day for both of us. So, do you want to kick things off? What's new in the world of the stablecoin bill?

The GENIUS act of 2025

Zeke: Well, as we speak, I think there's a hearing going on in the house where they're talking about this bipartisan stablecoin bill, which they call the GENIUS bill.

[Patrick notes: One of these days we will learn our lesson about forced acronyms. Today… is not that day. On the plus side, I can look forward to describing acts of GENIUS on Twitter.

The sponsors have so some comments on the bill which are easier for lay readers than the text itself, if that floats your boat.]

Zeke:

This is the Guiding and Establishing National Innovation for US Stablecoins of 2025 Act, which forms the acronym GENIUS Act. It's sponsored by Tim Scott, who's the chair of the Senate Banking Committee, and Kirsten Gillibrand, who's a Democrat from New York. So there seems to be some support for it.

Basically, it's going to require stablecoins to hold safe assets and to publish audits. If you don't know what stablecoins are, these are cryptocurrencies that are supposed to be backed one-to-one with dollars in a bank somewhere. The most popular one, which was a big part of my book "Number Go Up," was - or still is - Tether. Right now there's more than 130 billion worth of Tether outstanding.

Tether's audit controversy

There's also a rival stablecoin called USDC, which is issued by a US company called Circle. Circle would likely have little trouble complying with this stablecoin law since they already are publishing these audits. [Patrick notes: I concur with respect to the part which is about composition and disclosability of the reserves, but for what it is worth, there are other requirements. That said, if you had to pick which of the two has any prayer of complying…] But Tether famously has always said that they are about to publish an audit but have never done so, and only put out these lesser documents called attestation reports.

Patrick: And Tether has been saying that about the audit since, if I remember off the top of my head, 2017. It was a month away… and it's been 1 to 3 months away since 2017. [Patrick notes: 2017 is accurate; their forecast timeline changes periodically.]

Zeke: Yeah. And their claim is that the big auditing firms do not want to take the risk of signing off on Tether. I'm a bit skeptical of that. I feel like service providers will take on clients - they might ask for hazard pay if they think it's dangerous. What do you think?

Patrick: I think Tether also said at one point that one of the firms they approached was asking [Patrick notes: following is a paraphrase] "intrusive questions that they didn't need answers for."

My read on that - for folks who have never worked in an audit firm, and I've never worked in an audit firm, but I have some reading knowledge of how this works - they need to understand how you do business so they can probe at the controls of the business. This allows them to represent that the combination of statements they have from management and testing of things on a transaction level actually materially represent the financial health of the firm, and that the numbers published in the report are believable by interested parties up to some standard.

So these would be extremely basic things like "Tell me about your internal controls" and "Who is sending you money and how do you know when that money arrives that it is the amount you were expecting?" A

And when Tether's character witness, one Sam Bankman-Fried, went on Bloomberg Odd Lots [Patrick notes: transcript (Bloomberg paywall); Spotify link] to discuss how Tether did issuance from his perspective, he said - and not to put words in Sam Bankman-Fried's mouth because he had many words to say about it - but I will paraphrase that they're extremely attentive to DMs but the processes are just a little bit weird and cowboy compared to USDC, which was a comparison he explicitly made.

[Patrick notes: Bloomberg does verbatim transcripts, and you can read it by Ctrl-F “Like, can you do it? You can do it.”, but I think that quoting someone with the included level of disfluencies is below my personal standards, and so I will take the liberty of editing SBF’s remarks in the fashion I would edit my own. (I have, at some times in my life, had a speech impediment, and I am acutely aware that there are conditions under which a verbatim transcript of my speech would not redound to my favor.)

Can you do [redeem Tether]? You can do it. We have done billions but it's a messy process. It works, but, compare it to redeeming USDC. They have their U.S. dollars in a U.S. bank account, at the same bank that everyone else in crypto uses. It takes thirty seconds to create a book transfer, and then 30 seconds later, they send you your USDC. You can redeem them 30 seconds later, and they will immediately transfer you good funds. No fees are charged. It is a straightforward and smooth process.

Compare to Tether: it’s a messy process. Every piece of mess in the process makes it harder for them to present as having a self-evidently reasonable process. It gives you a heightened sense that something weird is going on.

Patrick elaborates: The bank that everyone at crypto banked at was Silvergate Bank. It is no longer with us. The real-time settlement API that Silvergate made available, the Silvergate Exchange Network, enabled more than $1 trillion of unsurveilled transactions, including by SBF et al. See Debanking (and Debunking?)’s discussion of Silvergate’s windup.]

Zeke: And let's just say if Sam Bankman-Fried is saying that your internal processes are subpar - this is a guy whose payment systems ran on emojis and who was actually stealing all of his customers' money using those emojis. So it's not a very good endorsement.

Patrick: I have to defend the honor of FTX on this narrow point because I do think that plausibly you can run a compliant expense reporting system on Slack using emojis if you have audit logs enabled. And depending on the nature of the risk and totality of controls of the business involved, that could be reasonable for a startup.

Zeke: Maybe a better criticism - this was a guy who, when his firm was going bankrupt, found bank accounts that he had forgotten about that held hundreds of millions of dollars.

Patrick: Yeah. And whose primary accounting software was some combination of QuickBooks and Google Spreadsheets, and who had eight candidate balance sheets depending on the needs of the moment.

The origins and impact of Tether

Zeke: Well, I want to roll this back a little bit because I feel like Tether is what brought us together. If you haven't heard of Tether, it's really a very funny company. It's what got me into this - I'm not a crypto reporter. I've always wanted to write an adventurous nonfiction book, and crypto just sort of came to me as this opportunity to do it. And it came through Tether.

My boss in 2021, the editor of BusinessWeek, asked me what I knew about it - he thought it might be a good story. When I started looking into it, I was shocked. At that point it was much smaller, but they still had more than 50 billion tethers outstanding. So if they're supposed to have 50 billion in the bank somewhere, but you'd ask these people about Tether in the industry, and they would say, "Oh yeah, Tether, yeah, I use it every day. I send and receive billions of dollars of Tether, but yeah, it's super sketchy. Could it be run by the CIA?"

Patrick: I'm glad you said that because it's been darkly hinted in many quarters that this is clearly an intelligence asset and that's why they're protected. But many explanations that people have advanced - or hypotheses more than explanations - don't have the ring of truth to me.

What does have the ring of truth is that there are epiphenomena to many industries that collect characters that are on a spectrum from "kind of weirdo but basically harmless" to "other than salubrious" to "parasites or criminals," and Tether is somewhere on that spectrum. I think everybody would agree. I said pretty confidently back in 2019 that they're the largest fraud since Madoff - that has now been decisively disproven because they're larger than Madoff ever was.

[Patrick notes: Was that the first time I had the thought? No. It was the first time I could beat the libel suit. See some hashed predictions for earlier versions of the thought evolving over time.]

Investigative reporting and red flags

Zeke: I want to get into that. When I started looking into Tether, one of the things that attracted me to it was I found a lot of crypto kind of impenetrable, but with Tether, the question was: do they have this money? They say they got 50 billion, but they won't prove it. And there's a lot of evidence that they've been lying about it in the past.

In your review - and thank you for the very thoughtful review of the book, it really meant a lot to me. One of the coolest parts about writing a book is seeing people engage with it. I actually enjoyed your criticisms of it too. But you talk about the role of investigative reporters. Actually, what I found is that a lot of times what people think the investigative reporter is going to totally nail everything. But often what the investigative reporter does is merely point out some of the red flags. And once they've done that, that sparks someone with subpoena power to do a bigger investigation. The stories that are credited with exposing the Enron fraud were actually very mild.

[Patrick notes: Extremely common for all sorts of detection of malfeasance! One of the things which did Stephen Glass in was he described an event at a hotel, and when someone went to that hotel, the physical layout of the hotel was incompatible with his description.]

Patrick: As I wrote in the book review, you have the best line about Tether from one of your early pieces on it. I think it was "Anyone Seen Tether's Billions?" And I'm a man who doesn't experience jealousy often in life, but I experienced jealousy for not having written this line: "Tether is quilted out of red flags."

But it's true - they jumped off a tree of nonsense and hit every branch on the way down. They say things like "we are fully reserved and have 100 percent adequate liquidity over any 24-hour window in our history," which is mind-blowing. One, that you would think that is adequate. Two, that you would say that. They denied for years that they were holding billions of dollars of Chinese commercial paper because billions of dollars of Chinese commercial paper are not necessarily one-to-one swappable for U.S. dollars in all environments, to put it mildly. And then it turned out, "Okay, yeah, we were holding billions of dollars of Chinese commercial paper, but what of it? Now our money is at Cantor Fitzgerald."

And then Cantor Fitzgerald CEO, Howard Lutnick - also a character - gave what I would describe [Patrick notes: and did, contemporaneously, describe] as an extraordinary vouching for them, saying in front of an audience essentially, "Questions have been swirling for years. Do they have all the money? I've seen so much stuff." This is not a quote, this is a paraphrase, but it's pretty close: "Our team has seen so much stuff. I'm telling you, they've got it."

[Patrick notes: Per Bloomberg Television, the quote: They have the money they say they have. … I’ve seen a whole lot and the firm has seen a whole lot and they have the money. And so there has always been a lot of talk ‘Do they have it or not?’ and I am here with you guys and, I am telling you, we have seen it and they have it.

]

Patrick: When I read that, I thought: if you asked Jamie Dimon, "Does Bank of America have all the money?" …

Under no circumstances is Jamie Dimon going to say "Yeah, please sign me up for every variety of liability if Bank of America ever screws up on anything in the future." No, he's going to say something anodyne like "Bank of America's a huge institution, well regarded, and extensively regulated. With regards to the portions of business that they do with us, we've underwritten them to our standards." And then if you probe them on it and say "But do they have all the money?" he's got to say "What didn't you understand the first time?” and think “I’m not stupid enough to sign up for liability down the line."

But Cantor was like "Yeah, they've got it all." And that got walked back during the hearings for Howard Lutnick, the CEO of Cantor. He's got ambitions and wants to be a member of the new administration, and so was going through hearings and got asked essentially "So it kind of seems like you've alleged that Cantor has ongoing extended due diligence of Tether, do you?" And he said "I believed my statements were true when they were made, but we don't have ongoing due diligence." Again, not a quote, but a paraphrase.

[Patrick notes: Per CoinDesk referencing a published transcript: Cantor Fitzgerald is not conducting continuous diligence on Tether’s financial statements, but I believe my statements were accurate when made.]

Zeke: When I started looking into Tether, they had far less vouching going on. They wouldn't tell me where they were keeping their money. And they had a CEO that had been seen so little that people actually speculated that he was made up and didn't exist.

Patrick: Yeah. They had the best red flag in the history of the financial industry, I thought, which is in various official documents, the name of their chief investment officer was redacted with the explanation being that we feared the discovery of the name of our chief investment officer.

Zeke: I missed that! [Patrick notes: Credit due to Bennett Tomlin, of the Crypto Critics Corner podcast, for spotting it.]

Tether's shady business practices

Zeke: The more I looked into Tether, the more concerned I became about what people were using the stablecoin for, and that search brought me to Cambodia where I was looking into Tether's use in these pig butchering scams, which are happening on a massive scale and leading to thousands of people being trafficked to work in scam compounds.

Patrick: Do you mind if I give the quick voiceover for a moment on what a pig butchering scam is? I think it's interesting that we took the words "pig butchering" - it comes from a Chinese expression. And sometimes the translators of Chinese expressions go in an overly literal direction, and we adopt that for whatever reason. Another example of this was "human flesh search engine" from a bunch of years ago, which was the Chinese equivalent of cancel culture with online mobs. That phrase was popular in US media for a couple of years and died out.

So right now we've got pig butchering. But pig butchering is essentially a very old genre of scam, which starts with you approaching a mark with some combination of romantic overtures or "I want to be your new best pen pal." There are many lonely people in the world, many people who want someone to love them. You gain your mark's trust via any number of untrue things you could say to them, or entirely anodyne things. And then eventually at some point during the conversation, you talk about the new hobby that you've been engaging in, which is cryptocurrency speculation. And it turns out you're quite good at it.

Patrick: And then what happens exactly next varies with the flavor text of the scam, but you invite your new best friend to co-invest with you in cryptocurrency. And then you tell them the easiest way to buy Tether in your country is to go to such-and-such and click the following set of buttons. And they do, and they send you Tether, and now they have your money.

Zeke: People are sending - I mean, billions of dollars are being lost to these scams. It's really taken off in the last couple of years.

Patrick: We lost a bank over this too. It's not just that people have this image of fraud victims as being unsophisticated, perhaps dealing with the challenges of aging, on the socioeconomic margins - all of that is true. You are at elevated risk for fraud if you have risk factors like those. However, the CEO of a bank is not naturally someone that you expect to fall for a scam that we have just described that might sound transparent to sophisticated people. And yet the CEO of a bank did fall for the scam and took the bank depositors' money and sent it to Hong Kong.

And this was discovered when he went to a buddy of his who was a farmer and customer of the bank. He didn't say "Hey I need a little bit of money to cover the liquidity needs in my bank" - he said something like "Can you give me a little bit of money? I need it for reasons." And the farmer thought this seems a little odd. And he goes into the bank and says, "I think the bank might not have the money." And one thing leads to another and now this gentleman is going to be a guest of the federal government for a while and the bank has been closed.

Zeke: Yeah, this is Shan Hanes of Heartland Tri-State Bank in Elkhart, Kansas. He embezzled $47 million and sent it to these scammers. Now, to be clear, these are not done exclusively through crypto - mostly through wire transfers.

I wanted to - this was a very long wind up to what I was trying to say - I became convinced that Tether was used for a lot of bad guys to do bad things. But I found Lutnick's vouching for Tether to be fairly convincing. [Patrick notes: I believe it convincing with respect to the portion of assets custodied at Cantor Fitzgerald, and have no reason to credit it with much of anything for the rest of the reserve.]

When Tether was investing in Chinese commercial paper, it was because interest rates were at zero, and they didn't have a great way of making money with their giant pile of reserves. Now they can invest in U.S. treasuries and clip 5%, which is what they say they're doing. So even if Tether had a fairly large hole a couple of years ago, which we don't have any proof of, they could have earned their way out of it by now. So I'm more inclined to believe that they do have all the money now. Even though I think their reluctance to provide the audit is because it would turn up something else they don't want to show.

Patrick: Yeah. And the nature of financial records is that they create long records of shenanigans in places that are extremely responsive to requests from law enforcement for those records. And then some of the lies you tell - even if you have all the money now, does that absolve me of all frauds I've committed in the past? Run it by your lawyers, but odds are not great.

But if I can give a slightly different hypothesis than the one you just advanced: You say you think that they had a bunch of Chinese commercial paper because they were in a search for yield and that was where the yield was, and now the treasury has yield so they've got treasuries. I think that they had a bunch of Chinese commercial paper because they had money in the wrong part of the world and couldn't get it onshore to the US, so they were looking for dollar-denominated essentially Eurodollars elsewhere in the world.

[Patrick notes: A eurodollar is dollar-denominated deposit liability at a non-U.S. bank. You can buy eurodollars from e.g. Japanese banks; I have from time to time owned some. Most are “in” places like London. You can also buy euroeuros, which are, you guessed it, euros that are not in the eurozone. Bloomberg’s Odd Lots has had a great series on the eurodollar system with Columbia law professor Lev Menand: origins, policy response, and hiccups along the way. ]

Based on where the money started within their network - the Bitfinex user base, the businesses in Hong Kong that were trading lots of cash over the counter - they ended up dealing with Chinese counterparties. And then there's no swift way to change commercial paper issued by, for example, Chinese banks, into treasuries. There needs to be a wire transfer at some point, and Tether had been blocked from sending wires from its proxy banks to the United States.

Zeke: This is where - one of the things that you pointed out in the review - the book, trying to keep the audience entertained, does not give all of the details of some of the financial things. One of those things is that if I remember correctly, even these Chinese notes were held in the Bahamas where they also could have held other types of assets. So I had the same theory that maybe they had money in China that they had to invest, but I came not to think that was the case. But I do think it's plausible, makes a lot of sense.

Tether meets SBF

Patrick: I do think that one of the turning points for that business was meeting Sam Bankman-Fried. You know, Tether quilted out of red flags. SBF et al: not obviously so.

I think people overemphasize SBF's role in the FTX/Alameda crime complex and under-emphasize that there's an entire power structure there, including both the core conspirators but also others that were materially involved with various levels of knowledge of the crimes.

Be that as it may, SBF looked very trustworthy for a number of years, was a rising star in American politics, noted philanthropist, looked to be making money hand over fist by being a pretty cynical exploiter, but a valued financial services provider to the cryptocurrency industry. And importantly, read as American upper class - his parents were professors at Stanford, he went to MIT, he was at a well-regarded trading firm for a while, knows all the right things to say to compliance departments in a way that Tether always says the wrong thing to compliance departments.

As a result, I think he was much more capable of directly accessing the U.S. financial system than Tether was. When I say I think - we have abundant evidence that he was much more successful at accessing the U.S. financial system. And so, I think that it is extremely likely that that confluence of interests allowed Tether to onshore more of its assets to the United States through Cantor rather than merely keeping them in various entities in the Bahamas. Having US-denominated assets in the Bahamas - that is not intrinsically a wrong thing. There's a lot of offshore finance that happens in offshore finance centers, and much of it is not bent.

[Patrick notes: There is a fairly common structure for U.S.-based VC funds which want to allow international LPs to invest without complicating their lives: put the international LPs in a sidecar vehicle in the Bahamas, and have that entity invest in the fund. Talk to your lawyers, but this is pretty bog standard, including by some of the best known VC funds in the industry as well as some funds that I am personally a tiny LP in.]

Patrick: There are a couple of offshore finance centers that have done a great job over the last couple of decades of cleaning up their act. But if you look at Sam Bankman-Fried prior to November of 2022, you don't see a massive risk. You see someone like, "Okay, this guy and his firm have almost 50 money transmitter licenses in the United States. [Patrick notes: By my contemporaneous impression, in every state where MTLs are a thing.] He's on the cover of Forbes. He's buying sports stadium naming rights left and right. It looks pretty legit, just a rich finance type." And then we learned what we learned.

[Patrick notes: There is a saying among communications professionals in the tech industry: if you are very lucky, you will get one Forbes cover. And if you are not, you will get two.]

New anecdotes in the Number Go Up paperback

Zeke: I put out an updated version of the book a few months ago in paperback, which you may not have seen since you've already read it. But there was actually some new intel from a lawsuit that I think you'd find interesting. So the boss of Tether is Giancarlo Devasini, who's this reclusive Italian guy, used to be a plastic surgeon. He's a very funny character. I found when he was - he's about 60 now - when he was younger and newly divorced, he kept a horny blog under a pseudonym that I found, where he also wrote somewhat with envy about Bernie Madoff, which I just thought was wild when I found it.

Patrick: I thought that was in the edition that I read, although I didn't read it on paper.

Zeke: So there was a lawsuit against Deltec Bank, which was Tether and Alameda's bank in the Bahamas. This is a lawsuit filed on behalf of FTX's customers to get more money back for FTX's customers. What they alleged was that Alameda got special terms from Deltec that allowed the fund to get Tethers kind of on credit for a couple days, which was actually really good for them because they were selling Tethers into the market at a slight premium. So it's very handy to not pay for them.

Patrick: So my recollection of this lawsuit - and I suppose, why does this matter? Tether has always said that we only issue Tethers in return for cash, which was pretty obviously a lie at many points, but it was a lie that they kept to for a number of years. And I think Caroline Ellison probably said like, "No, actually we have this relationship with Deltec where Deltec gives us a revolving line of credit of up to, I think, 2 billion or so where we express our intention to buy 2 billion worth of Tethers." Deltec gives Tether 2 billion via a book transfer at the company immediately coming from Deltec's money. We get our Tethers, we sell them into the market, we get money. And then within three days, we settle up with Deltec for this line of credit.

Zeke: My favorite part of this - and yes, Caroline Ellison cooperated, so that's how the lawyers have all this info - there was a group chat with Alameda's traders, some executives from Deltec, and Giancarlo Devasini. Where they would celebrate as Tether grew. And at one point an FTX person wrote "money for Sam has traditionally equaled money for Giancarlo, so all around good." And then Giancarlo wrote back, "We are a big family. We will conquer the world."

And FTX was not even Tether's only terrible business partner. Looking into Tether brought me to look into so many crypto frauds. And so it was truly amazing to me that Tether walked away from the last crypto bubble as a big winner. And now they just said that they made 13 billion of profit last year with something like a hundred employees. And I don't know if you saw the latest, but they are planning to move to El Salvador and build the tallest building in El Salvador - it's going to be a 70-story Tether tower.

And the Wall Street Journal has done some really good coverage of Tether in the last year or so. One of the things they wrote was that Giancarlo has talked about making this deal with Howard Lutnick of Cantor as a way of gaining favor with the Trump administration. Which might have seemed far-fetched a year or two ago, but now Lutnick was one of Trump's biggest donors and is in line to be the commerce secretary, which traditionally doesn't have much to do with crypto, but he'll be in the cabinet. And assuming he doesn't recuse himself, he's actually part of Trump's crypto council or whatever he calls it.

Patrick: I think that's also not the only politically connected to a large world power Tether affiliate - as I recall, they have a major shareholder of Tether/Bitfinex that's extremely involved in UK politics.

Zeke: Yes, this guy Chris Harborne who's a shareholder and was... yeah, I don't actually know too much about him off the top of my head, except that I remember that he sued the Wall Street Journal for defamation. So I will not attempt to freestyle about Chris Harborne.

Patrick: No worries. I know how it goes. And we'll talk about it more later, but the pluses and minuses of having major institutional backing... I assume that some other outlets in the world have much better lawyers than I do, so we will keep our noses performatively clean here.

At any rate, we talked about Tether having customers and I think it's useful to say - prior to returning to a broader stablecoin discussion - that Tether's perspective has always been that Tether has customers that actually transact with Tether directly. And it's a small number. I think they haven't been super public about how many there are, but the general sentiment is like 10, 20, something like that.

Then they have users and there's lots and lots of users. And Tether says, "Well, we've KYC'd (know your customer), we follow some level of diligence with respect to the people who transact with us directly. And then they sell the Tethers onto the secondary market. And after it hits the secondary market - well, what are we going to do? It's not like a farmer chases the corn they sell onto the secondary market all over the world. It's out of our hands."

Zeke: The reports, this is from various sources we've learned in the last year or so. Here are some people using Tether on the secondary market: Fentanyl suppliers in China, Chinese drug money launderers in the U.S., gold smugglers in Nepal, cocaine traffickers in Colombia, illegal casinos in Southeast Asia, an Irishman in Dubai selling fraudulent passports to Russians, Hamas, ISIS. And like you said, Tether's what they say is that unless you are buying Tether or Tethers from us for U.S. dollars, it's not really our problem.

And the way crypto works, it would be challenging for them to police some of this because you can hold Tether in your unhosted anonymous wallet. You can zap it around the world to a pig butchering scammer, and neither of you have to reveal your identity to anyone.

Patrick: And Tether's response to this has been, "Well, you know, we love cooperating with law enforcement here at Tether. And if law enforcement tells us an account to seize, we will certainly comply with that demand by law enforcement to seize an account.” But maybe they don't proactively go out looking for accounts to seize.

But what's your perspective on how candid is Tether being with that defense?

Zeke: They will seize accounts if instructed by law enforcement. And they do - they've seized accounts of scammers. But my take on that is that you have created this system that is enabling all sorts of bad things around the world. The criminals are speaking with their actions. They don't go use - I mean, using crypto is a hassle and these aren't like, you know, criminals don't tend to be the most sophisticated financially - they're all like, "This Tether thing is really handy."

There was a great intercepted message sent by some sort of Russian money launderer, where he's like, "It's so fast, it's just like email, but the money goes there and you don't have to use your name" or something like that. He's trying to sell his co-conspirator on why they should use Tether. And so I think when Tether - because they created the system - they bear some responsibility for it. And it's not fair to just say - any financial company would love to outsource all of their anti-money laundering responsibilities to law enforcement. And that's not how it works for other companies.

I would - correct me if I'm wrong, but when PayPal started, they didn't want to collect user information, right? Like I think the original plan was just emails.

Patrick: Yeah, back in the day, there were a number of contemporaries of PayPal that were all trying to do electronic money. And let's say there was a spectrum of desire to comply with laws versus be like the maximally usable internet thing. And most people have forgotten the names of the also-rans like Flooz, for example - "We're going to give Flooz to the entire world and you won't buy things with dollars anymore, you'll buy it with Flooz and we'll sell you Flooz for dollars." [Patrick notes: Sophisticated crypto financial professionals would say Flooz failed because it was a premined altcoin with a poor airdrop strategy and an n=1 validator set.]

PayPal was one of several companies with essentially the same thesis. And that was the one that figured out how to do it in a time of the internet which was like massive amounts of fraud were happening, and they figured out a legitimate business that was able to eventually handle all the responsibilities and grew to a global footprint.

[Patrick notes: I was a long-time user of Paypal to feed my family. Well, OK, during the period when I was a heavy user, I was the only member of my household. But can confirm: very useful for selling software around the world from Japan. Some years later I worked for Stripe, and am still an advisor there. Stripe does not endorse everything I say in my public spaces, but I do think that broadly they are extremely appreciative of Paypal paving the way for much online commerce.]

Patrick: Another contemporary early in the life of the Internet was this business called Liberty Reserve. And even as a student who knew nothing about anything back in those days, I took one look at the website for Liberty Reserve and I was like, "Oh wow, well, we're not in Kansas anymore." And so when people say that there's massive innovation happening in stablecoins to enable low-KYC euro dollars - externally back in my day, we walked uphill both ways to school, and since we hadn't invented slow databases yet, we put our stablecoins in a fast database.

Zeke: Yeah. So Liberty Reserve was essentially similar to PayPal, but it did not collect your information and it wasn't crypto. All the data was in one database kept by this guy from Brooklyn named Arthur Budovsky, and it was incredibly popular with criminals.

Patrick: And they recapitulated - well, I was going to say they recapitulated crypto's architecture, but crypto really recapitulated their architecture. They have the central organizer, Liberty Reserve, that keeps the database of who has all the money. And then they had, I think they called them changers, which are essentially analogous to cryptocurrency exchanges, where this is the business that is actually going to turn the database entry into cash or some other sort of value. And then the changers will interact directly with the Liberty Reserve's database to say, "Okay, you and I are going to do some internet hawala out of band. And then I'll settle up for you by crediting your omnibus account at Liberty Reserve with 200,000" or whatever.

Zeke: Yeah. I mean, Liberty Reserve used the same argument that Tether uses. They said, "We KYC all our changers. Those are our only customers. We can't control what the anonymous people are doing with our Liberty Reserve dollars."

And this is for anyone listening who's like an aspiring journalist - this is one of my favorite things to do in journalism. So when I was writing about Tether the first time, I had some of these same questions about like, is this legal? What's the precedent for this? I remembered Liberty Reserve. It's always a lot more fun rather than lawyers - an interview with a lawyer is pretty boring. So I was like, we need to talk to the real expert about whether this is legal. So I wrote a letter to Liberty Reserve's founder who was serving a 20-year sentence in a Florida prison. And I explained what Tether was and that they had 50 billion and their whole system. And he wrote back to me, "The U.S. will come after Tether and do time. Almost feel sorry for them."

Patrick: I think this gentleman is extremely well calibrated with respect to his prediction of future actions. [Patrick notes: Tether has not been indicted by a grand jury in the United States District Court for the Southern District of New York, but not in the same way that you have not been indicted by a grand jury in the United States District Court for the Southern District of New York.]

Zeke: But the weird thing to me - and another expert I talked to that stuck with me was this crypto trader. He was on a podcast describing stablecoins and how they can be held in unhosted wallets. And he said something to the effect of, "It's kind of wild that this is allowed, that you can have these anonymous dollars. I think when regulators catch on, they'll ban this." And that hasn't been what's happened at all. And this stablecoin bill that we were talking about at the top would actually allow stablecoins to continue to be used in the same way that they are now. And there's actually really nothing that prevents the scammers, the sanctions evaders, whoever from using USDC, the U.S.-based stablecoin, to do whatever they want to do - it can similarly be moved anonymously.

Patrick: The sentiment in the community has often been the last couple of years: one, that USDC is likely perceived as being under more seizure risk than Tether is, and then two… is wild.

Everyone wants dollar exposure. They like the currency. But the cryptocurrency enthusiasts, both the people who have legitimate interest in it and the people who have illegitimate interest in it, were spooked by the SVB failure, which briefly caused USDC to break the peg. They were like, "Oh man, don't give us those tainted American banking dollars that could disappear at any time. We want the gold standard Tether dollar. We know those guys are good for it."

I'm laughing here because this sounds insane to me, and people profess to believe it.

[Patrick notes: In a hypothetical universe where SVB depositors had not gotten an extraordinary backstop by the FDIC, Circle would likely have been able to immediately backfill the lost deposits by doing a punishing equity raise in Circle. They would have felt enormous chagrin at this. Tether on the other hand does capital injections ad hoc all the time.]

Zeke: Yeah. It's been well documented that Tether in the past has engaged in really serious shenanigans with customer money.

Patrick: I remember the settlement with the New York attorney general said that they had done forensic testing of Tether's books. And for an 18-month testing period they could actually only substantiate reserves on 26-ish percent of days in the testing period.

[Patrick notes: I should really do what Bennett does and bring paper notes to podcasts, because Tether’s history of lies, distortions, and general malfeasance does tend to overwhelm my memory. The transaction testing was done by the OCC and the specific claim was:

As found in the order, Tether held sufficient fiat reserves in its accounts to back USDT tether tokens in circulation for only 27.6% of the days in a 26-month sample time period from 2016 through 2018.

I express apologies to Tether for underestimating the length of time they were able to keep this fraud going with those mechanisms, and additionally for understating the number of days they were fully reserved by approximately nine.]

The importance of AML and KYC rules

Zeke: Not the best track record. Do you think that I am being too much of a financial prude by saying that I think anti-money laundering and KYC rules are important and that it's kind of crazy to just create this way for everyone to get around them?

Patrick: I have a nuanced perspective on this and so I should make a disclaimer. I've previously worked at a well-regarded institution that certainly follows all of its compliance responsibilities, and part of working in the buttoned-up part of the financial industry is, one, you get compliance training and two, you're socialized into compliance as a performance, and you need to perform this ingratiating affect, and if you can't perform that affect, you're very bad at your job.

So I'm a bit of a rule follower. I'm a Japanese salaryman too, so that didn't hurt anything there. But the broader societal question whether AML and KYC at the current margin is the best of all possible policies for society, I think that is a legitimate topic for debate. I think you can very easily advance arguments against it. There are tensions on the things that society wants - AML/KYC compliance versus banking the unbanked versus ability to send money to your grandmother in Mexico.

My preference is that when we have tensions between things society wants, we resolve those tensions through the political process rather than just commit all the crimes and then get around the laws we don't like anymore.

Patrick: I will say that, one, I think it is extremely important that your book shows that oh man, there were terrible things happening in the world. I want to say both that the people doing the terrible things definitely get huge value out of Tether and other payment rails. But they also get huge value out of encrypted messaging apps and pervasively available Internet and a number of things. And I don't go from "Okay, criminals get huge value out of encrypted messaging apps" to thinking "Oh, well, encrypted messaging apps are bad."

So if there was like a huge legitimate use case for stablecoins where the portion of all illicit behavior happening on stablecoins was just about the size of the portion of illicit behavior in the economy, I'd be much more bullish on crypto than I am currently. I don't think that's been demonstrated yet, although the cryptocurrency community has certainly said for a number of years like, one, we're much bigger than we think you are - all of the data is public, pity that we don't seem to be able to add up those numbers in ways that make sense.

[Patrick notes: See my past writing on stablecoin mechanisms and use cases from 2022, which concludes:

Money market style stablecoins don’t look to me like the obvious future of money movement. But they’re an argument with executable computer code attached. There is at least some possibility that that argument produces a user experience compelling enough, at risks society can stomach, that something which looks somewhat like them might end up a large, enduring part of the landscape.

I don’t buy it, but some smart people do.

One such group of smart people recently in 2024/2025 invested heavily based on this belief. And this is where I get to invert my standard disclaimer: Stripe does not necessarily speak for me in their spaces. (It would be sort of alarming to be if we never disagreed on anything, because then the information value I add would be zero, which would suggest I could be optimized out of the Karnaugh map without consequence.)]

Patrick:

But two, this is like, "We're going to the moon, baby. This will be the way that everyone transacts in the future." And at that point, the fraud will be totally diluted by all the legitimate transactions happening on our rails.

Zeke: I feel like that's a good point about encrypted messaging or the Internet enabling bad stuff too, and not getting - I wouldn't be calling to stop that, but I think when it comes to my opinion is that when it comes to these talking to people in law enforcement, they find that these KYC and AML rules are helpful at identifying criminals, stopping crime. They're not 100 percent effective. The crypto people love to pull out examples where banks got in trouble for laundering drug money or stuff like that. But they're better than having anonymous accounts.

I mean, in Switzerland - I thought it was funny to see that a Swiss regulator put out this statement about stablecoins and they were like "We've been looking at this, it sounds very similar to the bad stuff all our banks used to do. This is illegal here. You can't have stablecoins."

Patrick: If I can tease out a nuance that I think is relatively well understood within the financial and law enforcement communities, but it's not understood outside of it: A lot of the point of the AML and KYC regime isn't to prevent. It's to stochastically interdict it, which means contingent on you deciding to commit crime in the economy, you're probably doing that for a reason, to gain resources or power or some sort of personal satisfaction. A lot of crime will want to touch money. If you touch money, we keep records of it forever. And then law enforcement will be able to query those records as an investigative thing to tie together all your identities, your co-conspirators, et cetera.

And then, so even if we don't prevent the crime, it will make our job of prosecuting it so much easier. And particularly in United States practice - the United States, to a degree that is larger than other major democracies, loves doing forfeiture of money that was the proceeds of crime. And so the existence of the KYC and AML regimes allows them to sort of broaden the net from the initial discovery of a particular crime to maximizing for the assets that they're allowed to seize.

At the same time, back when the Bank Secrecy Act was initially debated, I don't think you could have convinced the American populace "Hey, should we build a database of everybody in the country and what their addresses and where they bank and what their bank account number is?" And so we didn't do that.

But we created this suspicious activity report and currency transaction report regime which law enforcement will tell you very directly - it's a great proxy for having all of the accounts because we'll collect a lot of the accounts. And people who aren't committing crimes have nothing to worry about. [Patrick notes: Yes, they really do say this, virtually verbatim.] But the ones who are committing crimes, we will have all the data that we would hypothetically have in a world where we had full visibility into who owns all the accounts.

Financial privacy

Although if I was worried about financial privacy, I would worry more about like the credit reporting system, some of the private databases that make it so difficult to keep your address secret, even your physical address. And of course the cryptocurrency community has said "We have the obvious solution to financial privacy - we'll put all transactions in a publicly reachable database and then this will be wonderful." I know they've done some things with ZK-SNARKs and Monero and other quote-unquote privacy preserving coins since then, but since the one that makes all the money is the one that keeps all the records world readable... Like many things the crypto community says, they have a lot of desires in life, but when those desires conflict with number go up, they very consistently choose number go up.

Sam Bankman-Fried's conference in the Bahamas

Zeke: Yeah. That was sort of, I think, the lesson I learned from spending years looking into crypto people - there are a lot of smart people working on things that sound cool in crypto, but when it comes down to it and you look at what is the main activity going on, it's number go up. And I mean, one of my favorite examples of this, I was at Sam Bankman-Fried's big conference in the Bahamas, like his party at the height of his success just after his Super Bowl ad and Gisele was there. Michael Lewis interviewed him on stage.

Patrick: I think some obscure people like Bill Clinton and Tony Blair might have made an appearance there as well.

Zeke: Yes, which - side note - truly embarrassing. I mean, both for them, but Sam Bankman-Fried was so unprepared for his interview of Tony Blair and Bill Clinton, he was just sort of mumbling through this to the point that Bill Clinton sort of tried to - he gave him like a fatherly hand on the shoulder.

But I went to this conference and I found it so depressing because all of the ideas I heard were so dumb. And I was sitting with this one guy who was pitching me - I had a series of meetings with different crypto projects that were, they must have done business with Sam Bankman-Fried, that's why they were there. And this one guy described like a spaceship game where you could own your spaceship and use it, you could earn money somehow with your spaceship. And as an author, you want to be able to describe things. And I'm pretty nerdy. I like spaceships. So I'm like, "Cool, man, let's play your spaceship game. I want to play, give me a crypto spaceship." And he's like - at that point he had already sold 300 million of crypto spaceships - and he's like, "Whoa, the game does not exist. We've merely created the spaceships and you can like gamble on their price and lend and borrow against the spaceships. The game is years away."

Loot NFTs

Patrick: There was another project, Loot, which they said "We're going to tokenize magical items for a universe of fantasy-flavored games. And so you'll be able to buy a bag of holding or whatever, and port it between all the games you play. And you will own that bag of holding. If you ever get tired of the game you're playing, you can use it in a different game." And what is the actual thing they were selling? It was literally the words "bag of holding" and trading these bags of holding with each other for thousands of dollars.

I thought - one, I'm the person this pitch is supposed to work on. I do love my games, I do love my bags of holding. I've never felt like, in entering a new game, "Oh man, I don't have a good magic sword, there's such a scarcity of magic swords in the world," because, just talk to the DM and say, "Okay, you've got a magic sword now. What do you want to do with it?" And then have the actual interesting conversation.

Zeke: Those Loot NFTs, they peaked at $80,000 each and no art.

Patrick: $80,000. Yeah. "Floor price" was the magic word in NFT land, right? So there was a floor price - off the top of my head, I think that was - so maybe I will check that for the show notes, but just to explain for people who don't remember the NFT craze: a floor price meant that in a collection of artifacts and/or magical artifacts that was being sold by an NFT promoter, it was the lowest price of anything in the collection. And the various NFT promoters would say, "Well, our floor price is three ETH or whatever. So this is going to be super valuable. Their floor price is only two" and so on.

[Patrick notes: Loot’s peak floor price, 12.5 ETH, was about $50,000 at the time.]

Zeke: Yes. That was relevant for me when I decided that I needed to join the Bored Ape Yacht Club and the floor price, which you said was too far away from hardcore financial stuff for the book, but I enjoyed-

Patrick: The Bored Ape Yacht Club - there was obviously a lot of mind-altering chemicals happening in the vicinity of your reporting. We had Jimmy Fallon trying to take his hand as a cryptocurrency promoter. And all of that to me felt like obvious nonsense is happening, but obvious nonsense is obvious nonsense. I sort of feel like you know what you're getting into if you're going into that world, and I can't get too annoyed by it.

But another of your chapters talks about a company that became very popular in the Philippines for "I can't believe it's not Pokemon" and also "I can't believe it's not indentured servitude." Can you say a few words about - was their name Axie Infinity?

Axie Infinity: A case study

Zeke: Axie Infinity. Yeah. So I think some crypto people might accuse me of cherry-picking bad examples of crypto for my book. And I would say to this: no, I picked the most famous things in crypto at the time, and they turned out to be bad. And Axie was one of them. In 2021, this was the go-to example of how crypto was great in the real world. And basically you had to - the Axies were these little blobs that looked a bit like axolotls, the strange Mexican lizards. I have one downstairs by the way, very cool looking.

So you had to buy four Axies and then as you battled, they would earn the game's cryptocurrency, which was called Smooth Love Potions. And why would you want Smooth Love Potions? Well, you need them to breed your Axies. Why do you want your Axies to breed? To get Smooth Love Potions. So it didn't quite make sense, but it really took off - the price of Smooth Love Potions went up and there were more than a million people playing this game in the Philippines, which is where the craze was centered. And it got to the point that people were - they had digital serfs working for them. They would buy Axies for other people, the other people would sit there playing the game all day, earning Smooth Love Potions, and they'd get to keep half of them, and the other half would go to the king of their Axie team.

Patrick: This is called the "scholar system," as I recall, and I think it's important to note - very obviously, there's no economic value being created in this system. People are receiving a reward that is doled out by a computer every day. The only reason that reward is capped is because the computer will only give a certain number of Smooth Love Potions every day. The Smooth Love Potions are not scarce in nature. This is a thing that no one actually wants in the world.

Nobody in the Philippines was playing this because they're thinking "Oh, Diablo, Starcraft, Counter-Strike are just so boring. I got to get my Axie on." They are playing this because it looked for a while that you could earn an income which was a material number relative to the median income in the Philippines just by grinding for Smooth Love Potions every day. But since there is no actual economic purpose happening, no economic activity, this was unsustainable. And it should be unsustainable on first look, and this argument should be pretty knockdown. And yet Axie was treated as a serious business and not an obvious Ponzi scheme in a number of places.

Zeke: Can I read a quote to you? This is Packy McCormick, an investor who has a newsletter online: "One of the main criticisms of crypto so far is that it has no real world value or application, but Axie makes you reconsider what real world value is. Kids in the Philippines, Vietnam, Brazil, and beyond are applying for Axie scholarships like they would apply for college or a job, hoping to bend their trajectories upward." And he was not the only person saying nonsense like this. People would say "You got to look at Axie" but of course it crashed.

Patrick: I think there's some value in saying - what's the phrase from the Bible, examine the beam in one's own eye before removing the mote from another's. [Patrick notes: Luke 6:41-42]

So I'll say the tech industry - the real tech industry - did not cover itself in glory here. Axie was invested in by at least one extremely well-regarded VC shop, A16Z. Axie was covered, I will editorialize and say, relatively uncritically, by Bloomberg until it blew up. It didn't blow up, because how can it blow up? It's just artificial off-brand Pokémon. But of course, eventually the wheels fall off the bus, the value crashes, and-

Zeke: Not so fast. Oh wait. There was a pretty exciting blow up.

Patrick: Oh was it the hack of the bridge, or am I misremembering?

Zeke: Yes. So, incredibly - U.S. officials have said this bridge associated with Axie was hacked for 600 million of other cryptocurrencies and the U.S. government blames North Korea. And has said that this helped fund its nuclear weapons program.

Patrick: Can I voice over just for a second for people who have not gone into the crypto fever swamps? There are a variety of different chains you can be transacting on. Each chain is conceptually a database where money or other valuable (question mark) things can be. And since there is no one crypto ecosystem but crypto people want to be able to send their value between different chains, there are essentially computer programs that will allow you to switch things between chains. Those are called bridges. One of these bridges was hacked. And then the U.S. government says North Korea made off with the money.

Zeke: Yes. And I should say - you mentioned A16Z - they looked at it, they're like "Wow, this Axie thing is really signing up a lot of users. The growth chart looks unbelievable." They invested 152 million in it at a 3 billion valuation. The company that made Axie has said they did not intend to create a speculative bubble and they didn't promise anyone anything. But I thought it was sort of like similar to Tether - I thought "Hey, you guys made this game. You saw the speculative bubble forming in the Philippines. You did not do anything to stop it."

Crypto's real-world consequences

And when I went to the Philippines, with the help of a very enterprising and able research assistant named Guill Ramos, we tracked down a guy who was arguably patient zero who first happened to start playing Axie and spread it around his whole town. And it was wild to see - people had borrowed, they'd taken out loans to buy Axies. When this thing collapsed, it had real consequences for them. I met a woman who had - she was going to leave her kids with her in-laws and moved to Dubai to get a new job, partly to pay off her Axie losses. These are real people's lives. Real consequences in the real world, which crypto does not do a great job of owning up to.

Patrick: On the topic of things that I think communities I consider myself a member of deserve to have more reflection over: One of these things is that we have bent our professional skills and things that we are very good at, like doing internet-scale marketing campaigns and testing webpages against each other to see which is the optimum for getting people to transact, and we are deploying those skills against people who are much less well resourced than us, who don't have a team of PhDs examining the economic case for this, to essentially extract money out of poor people in the Philippines while saying that this is great.

And when it blows up, is there accountability? Is there a sense of guilt? Is there a reckoning of this effort? No, it's like "Oh well, man in the arena" - alright, onto the next one. And I love aspects of startup culture. I love that we allow somebody to build a SaaS app and okay, they don't get many customers, the company goes bankrupt, you dust yourself off, you go on to the next thing. When a business is selling services to other businesses and the servers get shut off before someone expects them to be, the amount of actual harm to people who are really not positioned in life to absorb that harm rounds to zero, de minimis.

And now we are - I don't want to lay every evil in the world at the foot of crypto by any means. The Dubai labor situation for immigrants is the Dubai labor situation for immigrants. But sending one more person into that situation as a result of crypto debts is unconscionable.

[Patrick notes: I have a thread on this from 2018, and I stand by every word.]

Regulation and financial safety

Zeke: This gets at something that I think about the financial system, which is that scamming is - and I'm not saying just in general - scamming is inefficient for the economy. It does not make sense for all of us to be on guard all the time about being scammed. If we all had to read all the fine print, things would come to a standstill, and it's actually good for capitalism if there's some sort of regulator who can ensure that the fine print is not so terrible so that we can sign it without reading it.

Patrick: One of the accomplishments of the Internet as a system, as an artifact, as a collection of industries was - there was a perception back in the day that the internet is a PVP zone. It's the wild west. There are hackers everywhere. They're going to take all your money if you ever show your face on the internet. And there would have been no e-commerce but for innovations like TLS encrypting the credit card when you send it over the wire, PayPal, et cetera. And the regulation - particularly the United States financial system like Regulation E, which says if you lose money, don't worry, by regulation has your back, and they will waterfall that out. I won't go entirely into my Regulation E explainer here, but see it in the show notes. [Patrick notes: Also available as a catchy song, with lyrics courtesy of me and vocals by Sono.] But broadly, it's like "Don't worry, even if the hackers grab your credit card, we will make you whole."

Patrick: Though it is safe to transact on the internet, it is safe to buy this thing from this bookstore named after a river in Brazil, it is safe to buy things from a firm that you've never transacted with. You don't need a phone number on somebody's website to do business with them. And that safe space that we created in this environment that was previously low trust is what allowed the internet economy to evolve. And substantially all of the economic value of the internet is downstream from those footholds of safety, in islands of safety in an ocean of uncertainty.

And if you say "No, we want there to be a separate bloody Hobbesian ocean where everyone is constantly on their guard all the time, where you can lose all of the money, where life savings vanish at the click of a button" - one, nobody should want to transact in that one when they still have the option of transacting in the other one, but two, it's just a brutal society to create.

Zeke: I was listening to a podcast interview with the incoming - yet to be confirmed - but incoming chairman of the SEC. And he was talking about his approach to regulation. He's more of a libertarian. And he said something to the effect of "Hey, people are going to lose all their money and that's their right." And I can sort of see that where it's like, okay, you don't want to be telling people what they can invest in, but I also just don't think it's good in a world where there's no punishment for scamming - it's a really profitable activity that a lot of people will engage in.

Patrick: It would not be good. It's also one which we will industrialize and blitzscale to the moon and we will create these rapacious machines to inflict this damage on people. I like Matt Levine's proposal that if he had a magic wand to wave at securities regulation, he would allow you to opt into stupid investments and you would have to go into the SEC's office and get punched in the face and be told you were opting into stupid investments. And then after that, you can lose all the money.

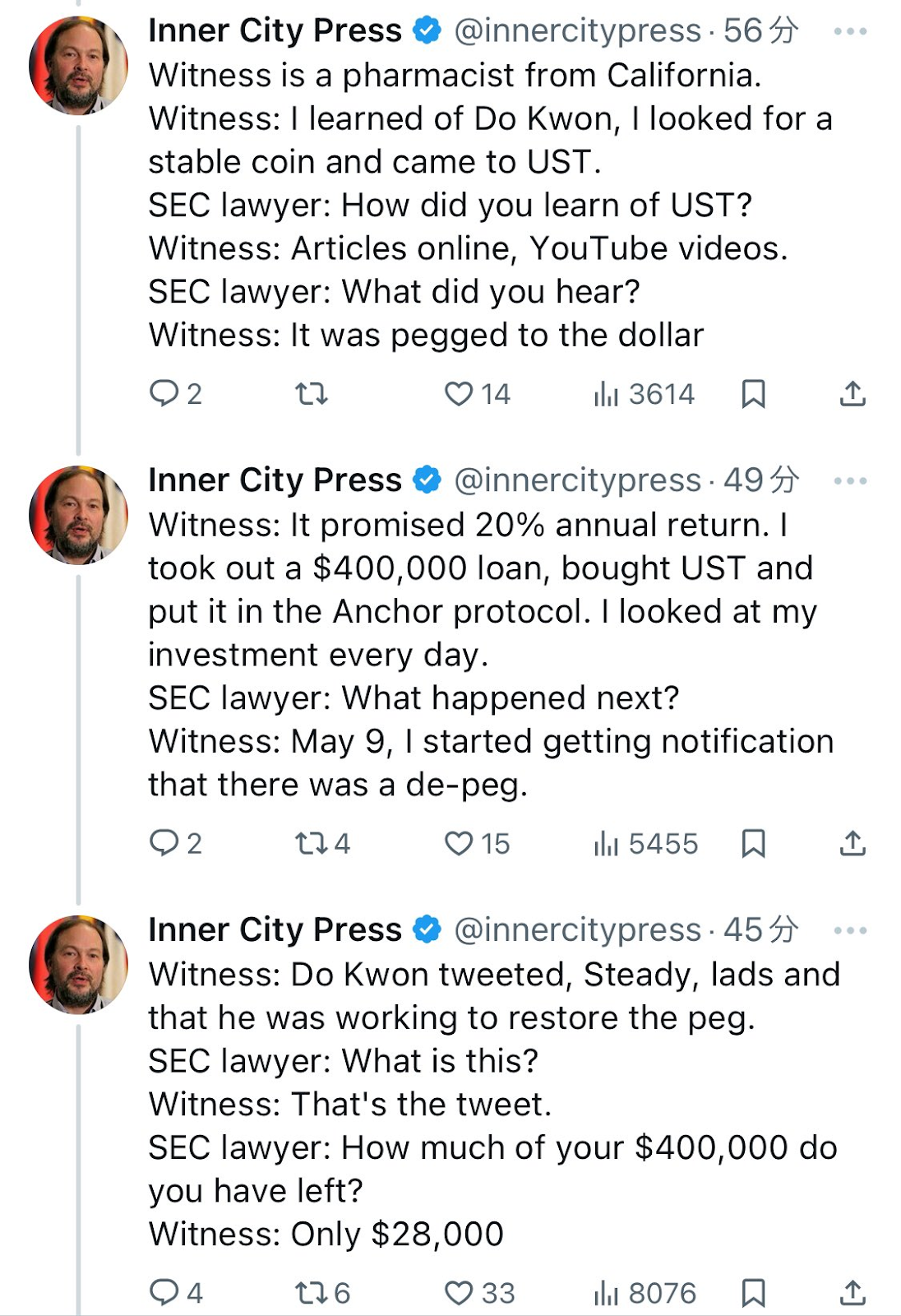

But the nature of securities regulation has historically been that if you allow fully 100 percent laissez-faire then moral outrages will be conducted against both the weakest members of the community and also not weak, not powerless, but very sympathetic members of the community at such a rate that it will be politically untenable to continue the laissez-faire. [Patrick notes: A classic example, from InnerCitiesPress recounting a court hearing on Terra/Luna.

]

And thus we ended up with some securities regulations. I don't have really strong opinions on whether our securities regulations are positive at the current margin in every direction. There are some places where it seems fairly obvious to me that we're not at the optimal place on the spectrum but, oh man, full-on laissez-faire is not in the interest of the consumer, it's not in the interest of capitalism either. I feel very strongly on that one.

Patrick: I used to be - perhaps some people don't know this about me - I used to have way too much time on the internet when I was a Japanese salaryman. And so I hung out on this forum for people that had problems with their banks and I would ghost write letters.

[Patrick notes: Yeah, really. I once won an award for it from the Motley Fool, under a pseudonym which is laughably transparent, so please don’t take that as a challenge to look up my adventures through my early twenties, Internets.]

And one of the things that - many people do not love banks. One of the things that created my early love in banks is oh man, they do all sorts of screwy things in the world, and I've written extensively about that in Bits About Money, but when you get through to someone whose title is Senior Vice President of Consumer Lending and you say "Hey, there is a grandmother in Kansas who is having a really rough go of it right now because your bank has screwed up. Can you please fix this?" they will actually fix it at a much higher probability than people would guess - particularly if you feel like banks are the number one source of evil in the world.

And I don't think we should lightly discard that. I don't think we should lightly discard that there are always going to be the police and the government, et cetera, but a purpose of financial regulation is to put people at every bank and similar in the country and say "Okay, your job is standing ready against every threat in the world that is coming after the life savings of a Kansan grandmother. And you're going to protect her from those. And if she nonetheless gets victimized, it's on you." And people I talked to can be in a really rough situation if you lose all the money. And the notion that they could actually have a procedural access to getting it back was much better than the alternative, I think.

Zeke: Yeah, totally.

Stablecoin bill and ownership limit

Patrick: So refocusing for just a moment on the stablecoin bill - I had one thing that jumped out at me was that the authors put on their webpage announcing it "We don't want bad actors to control a stablecoin issuer. So we will block them - if you are an XYZ bad actor, you've been convicted of money laundering or similar" they call out Sam Bankman-Fried by name - "you'll be allowed to own no more than 5 percent of the stablecoin issuer."

And when I read that, I thought "Wow." So I get what you're going for here. Another law that I'm pretty sure we have is that if you are a good actor, an upstanding pillar of your community, absolutely faultless in all things, a major philanthropist, you are allowed to own no more than 10 percent of a bank.

[Patrick notes: I slightly overstated this. There is a notice requirement at 10%, which gives your regulator option to reject. There is a hard cap at 25%.]

And so the margin that we seem to be enforcing here is that in stablecoins, if you are a convicted money launderer, then you're 50 percent as trustworthy as the town pastor.

Zeke: That is pretty funny.

Patrick: Seems just bizarre to me.

Zeke: Did they really name Sam Bankman-Fried in the law?

Patrick: Not in the law, but in the webpage announcing it he's definitely name-checked. By the way, so you mentioned this is bipartisan legislation. I think the thing that is underappreciated in the crypto community - I'm saying this not to make a partisan point, just trying to explain the world as I see it.

Political realignment and crypto

One of the reasons that the Democratic Party turned against crypto very rapidly after November 2022 was that SBF was perceived in Washington to be the heir to George Soros, the new well-moneyed standard bearer of the Democratic Party in the rising generation. And he was throwing his money around quite broadly while his cutout Ryan Salame was trying to sew up the other side of the aisle.

And one of the reasons the Democrats got very bearish on crypto after November 2022 was that they were attempting to performatively demonstrate that "Okay, he definitely tried to buy us, but he didn't successfully buy us." And there has been something of a political realignment with regards to crypto after that. And I do think people should understand - okay, there's a reason that they're a little bit POed and maybe it's not an entirely altruistic reason, they're attempting to buy some amount of for prior behavior that was inadvisable, but there's an explanation for this.

Zeke: Yes. And I don't - I think it - even if you don't, even if you're not being cynical about it, it makes a lot of sense. I mean, this guy was coming to testify in DC about how to regulate the crypto industry while running this hall of fame fraud.

Patrick: Well, you know, contrasting the regulation of the crypto industry that he was proposing with those idiots in tradfi who kept doing such blatantly inefficient things, like having separate separation of concerns.

Zeke: Yes. I mean, if the nuclear power plant CEO came to Congress, said all sorts of great things and then his plant melted down, you know, you would - it would not be surprising that they would be skeptical of the nuclear power plant CEO who came in. And it's actually been amazing to see how receptive they've been to crypto ever since the industry formed a super PAC and spent $150 million in the last election cycle - more than any other industry, I believe, which is amazing. It's a pretty small industry.

Patrick: I will trust your representation on that, but memo to self - put something in the show notes that compares this to other things because while the finance industry is often leading the lobbying lists in prior elections to my understanding because, go figure there's a lot of money flowing through finance, crypto beating out the financial industry and all other industries is a priori surprising to me based on how much economic activity happens there and what's the amount of government regulation and so on.

Zeke: They spent - the crypto industry spent something like 40 million on the Ohio Senate race defeating Sherrod Brown who was not even particularly outspoken about crypto but was believed, I mean, I think correctly to be an ally of the pro-regulation Congress people like Elizabeth Warren. And none of these crypto ads ever say crypto - they're spending all this money, but just advertising on unrelated things.

Patrick: Well, let's see - one final note for people. There was testimony heard by the Senate last week as of the recording of this podcast - I think it would have been on the 5th or 6th of February, we'll put the exact date in the show notes.

[Patrick notes: February 5th, Investigating the Real Impacts of Debanking in America.]

Patrick:But the testimony was on the subject of debanking, which has been heavily tied to the crypto narrative for the last few months as a result of crypto advocates in ways that I think they have some good points. Debanking is certainly - oh man, I don't want to recount my entire essay Debanking (and Debunking?). They have some good points. They have some arguments worth listening to. They also say some things which are extremely cynical and motivated to get them concessions that their businesses will benefit from.

But the hearing is pretty good - as something of a connoisseur of talk about this topic, some of the testimony there was in much more depth than you typically hear this addressed in the places that have been talking about debanking to this point, and much of it is, let's say, more reality-entangled than some of the stuff that you might see thrown out on television or places like Twitter. And so I commend that discussion to folks. I will drop a link here.

[Patrick notes: If you only watch one, watch the statement by Stephen Gannon. His prepared remarks are available.]

I think we could probably talk about this for another seven hours, but all good things must come to an end. Zeke, where can people find you online?

Zeke: You should look for me on Bluesky - just @ZekeFaux. And "Number Go Up" is available wherever you get your books. And I promise that I'm much more entertaining writing than talking. So if you like this, you'll like the book.

Patrick: "Number Go Up" is probably my favorite crypto book, and I'll drop a link to my review in the show notes. There are so many layers to the onion. Can I ask one question before I let you go? So you - I don't know if this is fair to your self-conception of it as a writer, but my perspective is there's a bit of gonzo-adjacent journalism happening where you seem to be self-consciously a character in the book, and we, the audience, are following you as you jaunt around the world and meet these great characters that are doing crazy things. And it seems to me that is a slightly different genre than usually happens in investigative journalism and storytelling.

Zeke: Yeah, I don't think I earned the adjective gonzo because I don't think - I mean, I guess the crypto world is gonzo, but I think I wasn't crazy enough to qualify. But I definitely thought that if I didn't put myself in the story, I would be leaving good material out of the book. And maybe one day someone could really do a forensic reconstruction of everything that happened at FTX, and that might be a really interesting book.

But what I wanted to tell the audience was the story of when I met Sam Bankman-Fried, and he shuffled into the room in his tube socks, without acknowledging me, pulled a packet of microwaveable chickpea korma from the shelf, and then without microwaving it, started spooning it into his mouth. To me, that sort of scene is priceless. Now could an author get that sort of scene by interviewing people who knew Sam Bankman-Fried and saying, "Hey, do you ever see him do something funny in the break room?" Like, yes, people do that. But I thought that given the timing of the book, it would be much better to be able to share my impressions. And also because some of the stuff was a little inconclusive, as you rightly point out in the review - like it was very interesting to finally meet the man who doesn't exist, Tether's CEO, but I didn't really learn a lot of facts from that. So I felt like the topic lent itself to first person.

Patrick: Knock on wood. I think the final chapter of that book has yet to be written, but we will see if it happens or not.

Zeke: I'm with you. I want to write one more chapter, but we'll see what it is.

Citizen journalists and the crypto-skeptic community

Patrick: So, one more final question. You're a serious journalist. You work for a serious publication that has a dedicated crypto practice among other things. But you bounce around on the internet, like many of us bounce around on the internet. You bounce around with me - I'm not a journalist per se, but let's say I'm a serious professional. And then there are other people that have been on this beat for a very long time that come from all walks of life. Some of them are sometimes described as trolls. I think some of them are - it would be much more fair to call them citizen journalists. If it were up to me, I would give them the Pulitzer at some point in the future. But what's your perspective on the relationship between "real" journalists and the, for lack of a better word, crypto skeptic community?

Zeke: Well, there's one particular character who we both know, goes by Bitfinex'ed on Twitter, who's been tweeting all sorts of skeptical things about Tether since before I was even looking into it.

Patrick: Also true of me - I would never have heard of Tether - well, I would probably have heard of it eventually, but the thing that originally put me onto Tether was Bitfinex'ed.

Zeke: They have made a lot of helpful points, and sometimes pointed me to things I wouldn't have found otherwise. They often go further with less evidence than I would feel comfortable with. But I find someone like that can be a good source of information. And also - it's not quite the same category - but there's mixed opinions about short selling. And I think I find short sellers' reports to be very interesting and to be a source of potential story ideas. Now, when I read them, I understand, "Hey, this person is trying to make their argument sound very strong so that the stock will go down and they'll make money." But that doesn't - they also were motivated to spend lots of money to send researchers to China to see if the factories were real. And even if I'm not going to take their word for anything, they could have insights into things that are going on that I wouldn't know about otherwise. So I really appreciate the citizen journalists, short sellers, the people who will entertain kind of things that might sound like conspiracy theories.

Patrick: I don't know how much detail I can go into on some of these things, but as someone who worked in the finance industry for real, I've gotten enormous value out of them. I think of them sort of like the Baker Street Irregulars - that Sherlock Holmes collection of orphans and so on that he was able to use to turn investigations into solving crimes on behalf of the actual government.

And I remember one particular conversation with an institution that shall remain nameless where I came to be in the position to tell them things that were acutely relevant to their interests.