The banking crisis, two years later

This week I'm solo in the studio. Back in March 2023 I wrote Banking in Very Uncertain Times at Bits about Money, my newsletter about the intersection of finance and technological infrastructure. Today's episode is the author's commentary on that essay, with the benefit of two years of hindsight, and spelling out some of the things that I couldn't say at the time (and the rationale for why).

I wanted the opportunity to do a bit of implicit meta-commentary on journalists, regulators, and randoms who write essays on the Internet. Some of us do keep score. It keeps me honest. (After action reports of e.g. regulators are linked below. Their honesty is... discussed in more detail, below.)

Sponsors

Vanta automates security compliance and builds trust, helping companies streamline ISO, SOC 2, and AI framework certifications. Learn more at https://vanta.com/complex

Support proven charities that deliver measurable results and learn how to maximize your charitable impact with GiveWell. Go to givewell.org (and type in "Complex Systems" at checkout).

Check is the leading payroll infrastructure provider and pioneer of embedded payroll. Check makes it easy for any SaaS platform to build a payroll business, and already powers 60+ popular platforms. Head to checkhq.com/complex and tell them patio11 sent you.

Timestamps

(00:00) Revisiting the March 2023 essay 'Banking in Uncertain Times'

(01:47) The Fed's study

(11:21) Why are banks failing?

(14:41) A useful heuristic from bond math

(18:05) Sponsors: Vanta | Check

(21:00) Maturity transformation

(29:54) Sponsor: GiveWell

(30:42) Liquidity problems are the proximate cause of bank failures

(33:43) Trying to forestall a banking crisis

(40:16) Deposit insurance expansion

(47:12) Deposit insurance has some legacy issues

(52:04) What would happen if my bank were to go into receivership this weekend?

(59:46) What should users of the banking system do?

(01:04:09) Parting thoughts

(01:05:08) Footnote

Transcript

Hi everyone, my name is Patrick McKenzie, better known as patio11 on the Internet.

I sometimes get asked if I'm a journalist, and the answer is mostly no, because I don't break news. That's largely an intentional choice - partly because it's not where I've put my character points in getting good at things, and partly because it's simply not what I choose to do with my publications.

For example, Bits About Money very intentionally almost never discusses anything happening uniquely this week. I try to write explainers about financial infrastructure - the cultural and technological underpinnings of why those complex systems fit together. But I don't usually ground those explanations in current events.

[Patrick notes: As I’ve previously remarked to Byrne Hobart, a few of us finance-adjacent writers have different strategies here. Byrne and Matt Levine often ground their ~daily columns in the news of the day, without generally reporting that news, per se. I have even less connection than that. While I’m occasionally moved to write by a news cycle, I’d prefer if almost everything I wrote retains value over ten years, and news depreciates straight off a cliff.]

My one exception is that I will occasionally cover current events when, given the nature of my beat, not covering the current event would itself be a very major decision.

Journalists sometimes flatter themselves and say that journalism - breaking news - is writing the first draft of history. But I will say, as a writer who has immense regard for journalism, that the first draft of most things is often very bad in retrospect. In most cases, we don't treat the first draft as a product we're emotionally attached to.

Let's examine my own work critically. I thought we could revisit some writing I did in 2023 during the early stages of the spring banking crisis and see how well it has held up given what we've learned over the intervening almost two years.

The Federal Reserve Study

What specifically prompted this review was reading an academic article recently published by the New York Federal Reserve. It was technically written in May 2024, though revised in December 2024. The paper is Tracing Bank Runs in Real Time, authored by Marco Cipriani, Thomas M. Eisenbach, and Anna Kovner.

This article is fascinating for two reasons. First, it presents an interesting approach to exploring bank run dynamics from a somewhat privileged point of view - they have access to data sources that are very difficult for outsiders to obtain. Second, it clarifies some uncertainties we had in March 2023 about what was actually happening.

Let me read you the abstract:

We use high-frequency interbank payments data to trace deposit flows from March 2023 and identify 22 banks that suffered a run significantly more than the two that failed, but fewer than the number with large negative stock returns. The runs were driven by a small number of large depositors and were correlated to weak balance sheet characteristics. However, we find evidence for the importance of coordination because run banks were disproportionately publicly traded and many banks with similarly bad fundamentals did not suffer a run. Banks survived the run by borrowing new funds and raising deposit rates, not by selling securities.

For those who don't read the full article (though I encourage you to do so), they specifically traced FedWire payments and ACH transfers between banks. The fundamental nature of a deposit run is that people want their money out of the bank.

Our image of deposit runs from "It's a Wonderful Life" - people sidling up to the teller window attempting to withdraw cash - is inaccurate. Most deposits stay within the banking system; they just flow to another bank. [Patrick notes: There is some risk that deposits could flow out of banks specifically to another place in the financial system and buy up non-deposit money-adjacent financial instruments, such as e.g. money market funds, but to do that, they do have to move in the financial system first, from e.g. a large regional bank to e.g. the money center bank which handles money movement on behalf of a large brokerage.]

Statistical Significance

There's a particularly striking line in the paper: "We identified 22 run banks with significant net liquidity outflows on one of the days between March 9th and March 14th, exceeding five standard deviations of their historical net outflows."

Five standard deviations - that's a heart-stopping number. For those who don't have statistics fresh in mind, let me break this down. In the universe of approximately 4,500 federally insured banks in the U.S. (plus about 4,500 credit unions), you should expect to see a five-standard-deviation outcome approximately once every 3.5 million observations, assuming normal distribution. This means you'd expect about four years between each bank experiencing a five-standard-deviation outflow.

Having twenty-two banks experience five-standard-deviation outcomes in just five days is, well... while "catastrophic" might be too strong a word (we did weather the crisis), it's certainly a heart-stopping statistical anomaly.

[Patrick notes: Intuitions about standard deviations often imply a normal distribution or a stochastic process which is uncorrelated between observations, and (very obviously) this assumption breaks down during banking crises and financial crises. A statement often made is that “all correlations go to one” in times of stress, though that is more an intuition than a claim about mathematics.]

Real-Time Understanding

A fascinating aspect of large distributed systems, even those run by people with arbitrarily large staffs of very intelligent people, is that sometimes you don't exactly understand what you're looking at in real time.

For context, let's review the timeline:

- Silvergate bank announces voluntary dissolution on March 8th, 2023

- Silicon Valley Bank failed on March 10th, 2023

- Signature Bank failed on March 12th, 2023 (over the weekend)

- I wrote my essay "Banking in Very Uncertain Times" on March 14th, 2023

To be precise about the timing, while we say colloquially that you wrote something as of a certain date, everything takes time to write. This was written over the weekend prior to the 14th but was ready for publication (or at least as ready as anything I write ever is) on the 14th when it started hitting people's inboxes.

The specific dates matter here - March 10th was a Friday, the 11th and 12th were the weekend, the 13th was Monday, and this came out Tuesday as my explainer for people worried about what they were seeing in the news.

[Patrick notes: The original essay, Banking in Very Uncertain Times, is of course available to read. I’ve taken the liberty of marking as inline commentary those portions of the below transcript which are substantially new. In the actual audio, I try to distinguish vocally or via explicit signposting (i.e. saying “Back to the essay”), but this is still something I’m working on.]

Understanding Bank Failures

Over the last week, three U.S. banks have failed. More banks are under extreme stress. This stress is not new and was not unknown but is becoming common knowledge rapidly. We may be in the early stages of a banking crisis.

Patrick comments: In my essay, I stated that three U.S. banks had failed. This requires some clarification, as officially only two banks had failed. "Fail" is a technical term in banking - it means your bank went bust and the FDIC needed to step in, invoke the deposit guarantee, and usually sell you to another bank over the weekend, in concert with your primary bank regulator (who's usually not the FDIC).

[Patrick notes: The sequence of events is generally an order from your primary regulator that you cease operations followed by the FDIC swinging into action. Your regulator has prepped the FDIC to receive the call, during the mid stages of the process which begins “Hmm that’s odd”, proceeds through “We are very worried about you and you need to be concerned”, and ends with the U.S. having one bank less than previously.]

Patrick comments: The third bank I referenced was Silvergate Bank - I affectionately called it the First National Bank of Crypto. Silvergate had wound up early in the week. What's the difference between a wind-up and a failure? You might say one is like the controlled demolition of a building versus the building just falling apart. Silvergate described their decision to wind down as voluntary at the time, though they've since characterized it as not entirely voluntary, alleging that banking regulators made demands incompatible with continuing operations. [Patrick notes: For much, much more on that subject, see Debanking (and Debunking?).]

Disclaimers and Context

I included a bold disclaimer in the essay: "This situation is evolving very rapidly, and this essay will not. Please check the WSJ or Financial Times for updates on the fluid bits. Hopefully this essay helps contextualize what is reported."

Patrick comments: This was an explicit acknowledgment that I'm not the news media and can't provide ongoing updates about breaking news.

I also included a disclosure about my background at Stripe: "I worked at Stripe, which is not a bank but works with many banks, for six years prior to leaving full-time employment recently. I'm an advisor there now. My views are entirely my own, and my analysis is informed only by publicly available data."

This disclaimer served two purposes. First, to avoid having my statements attributed to Stripe, obviously. Second, to clarify that I wasn't operating with privileged information. Some people, like Federal Reserve employees with access to Fedwire data, have privileged views of the financial ecosystem. Any commentary they make might reasonably be interpreted as informed by non-public, potentially newsworthy intraday settlement data between banks. [Patrick notes: And thus we responsible professionals have to disclaim floridly, in addition to prudentially avoiding comment on many things we would like to comment on, or which people would prefer we comment on.]

The Nature of Bank Failures

Why are banks failing? As we've previously covered regarding deposit insurance (now unfortunately topical), banks don't fail in a day. The seeds of their destruction are sown and watered for years, then reaped quickly. Importantly, these seeds don't come with warning labels.

People have a great desire for there to be a narrative here - for bank failure to require stupidity or malfeasance, or ideally, stupid malfeasance. But what's actually killing banks is a very simple idea with profound consequences: When interest rates rise, all asset prices must fall.

This is both almost a law of nature and perpetually underestimated in how much it affects the world beyond asset prices. For example, in January 2020, I pointed out on Twitter that engineering compensation includes an interest rate derivative because it includes equity. This isn't obvious to many people in tech, including financially sophisticated ones.

But equity isn't the only thing embedding an interest rate derivative - all prices do. The price of eggs embeds an interest rate derivative, among many other factors like grain costs. The price of grain embeds an interest rate derivative. The world sits atop four elephants who stand astride the risk-free rate, and then it's interest rates all the way down.

The Interest Rate Environment

The price of eggs and other important parts of the consumer basket is a major reason why we're here. The United States, through the Federal Reserve, made a considered decision to manage inflation by hiking interest rates. This is explicitly an intervention to push down the price of eggs and other things, via a lever that's more amenable to direct action than other available options for controlling prices.

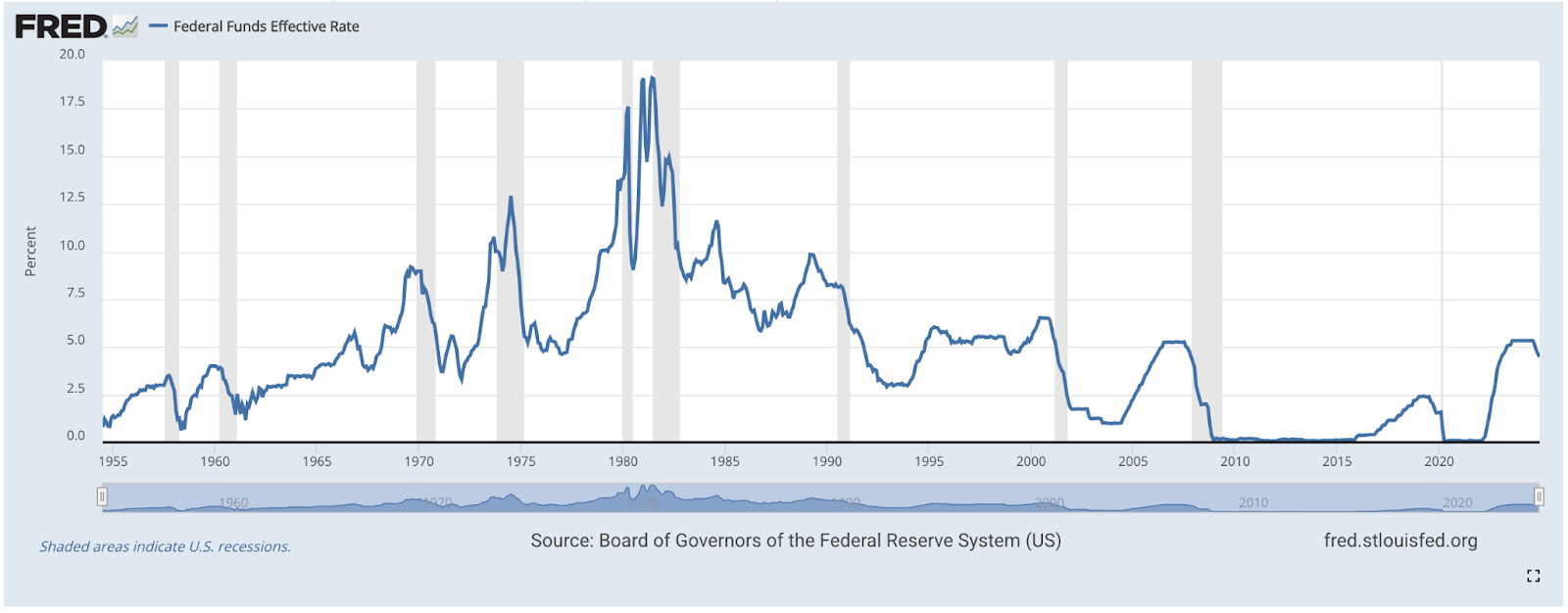

If you recall the past 15 months, we went from interest rates just above zero to almost 5%. This was the most aggressive rate hike since World War II, or put another way, in the history of the modern economic order.

Patrick comments: As an aside, that claim is somewhat glib. In 1980, there was a significant whipsaw in interest rates - the Fed funds rate went from 17.6% in April to 9.47% in June, then back up to 19.08% by January 1981. So by some measures, that was a more aggressive hike. But the claim is still defensible since rates weren't rising from nearly zero, and people had recent memory of comparable rates. See the Fed’s chart, below.

The decision to sharply manage down prices was, indirectly but inescapably, also a decision to cause large notional losses to all holders of financial assets. That includes everyone with a mortgage, every startup employee with equity, and every bank. That is the proximate cause of the banking crisis, if indeed we are in one.

Three banks failed first because, for idiosyncratic reasons, they were exposed to sudden demands for liquidity, which makes large declines in asset values unsurvivable. But many more banks have similar issues on their balance sheets.

Understanding Bond Math

Let me explain a useful heuristic from bond math. I apologize for this very basic financial math lesson, but it's unavoidable, useful, and may not have featured in your education. (And yes, Matt Levine beat me to mentioning this.)

There's a heuristic for the value of bonds: Every bond and every instrument created on top of bonds has a duration, which you can round to "how many years are left until we expect this to be paid back?" Every bond and instruments on top of bonds has a market price that moves down by 1% per year of duration if interest rates move up by 1% (and vice versa).

There is better math available, but this is math you can trivially perform in your head and is close enough to blow up large portions of a financial system. So if you held 10-year bonds and interest rates went up 4% in a year, your 10-year bonds are down somewhere in the 35%-ish range. This is true regardless of whether they're good bonds - if you want to sell them today, buyers have better options than you had a year ago. To induce them away from those better options, you need to give them a 35% discount.

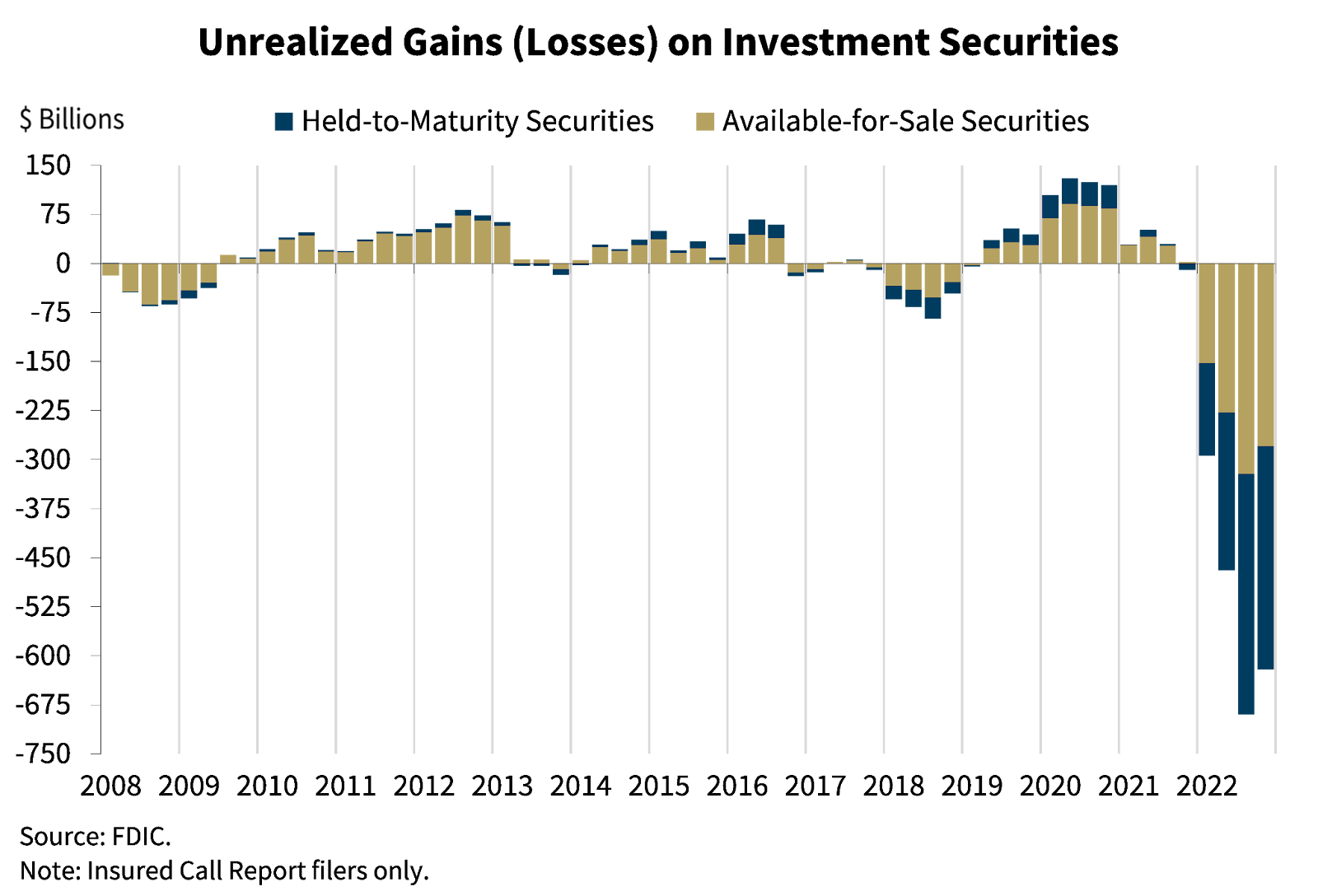

The Scale of Losses

We now come to one of the most important charts in the financial world, courtesy of the FDIC in February 2023. The U.S. banking system has $620 billion in unrealized losses on investment securities per the FDIC. $620 billion. That is a loss no less real than if the money had been loaned out to borrowers who defaulted.

It might be temporary - if interest rates go down, bond prices will recover (and sometimes defaulting borrowers receive an inheritance or get bailed out), but one doesn't generally want to count on that. For the moment, banks are out $620 billion, and the Fed recently signaled more aggressive rate hikes.

(As a side note on what actually happened with rates since March 2023: The Fed funds rate was at 4.65%, went up to about 5.33%, stayed there for a while, and recently came down to about 4.5%.)

Was this because banks invested in poor credit? No. The price of everything embeds an interest rate derivative, including definitionally perfect credit like U.S. Treasuries. The type of security most numerically relevant here is functionally immune to credit risk: agency-issued mortgage-backed securities.

You might remember that financial instrument from 2008. Many people are going to fixate on that coincidence far more than is warranted. In 2008, those embedded bad and mispriced credit risk, which had an uncertain backstop. In 2023, the losses are caused by bad and mispriced interest rate risk with a rapidly evolving backstop.

Some might ask: Why do banks buy exotic assets with lots of letters in the name, like MBS from GSEs? Why can't they just do banking - make regular loans to real people and businesses with income to service them? That would surely solve this, right?

No, it wouldn't. If they created fixed-rate loans - just plain vanilla loans warehoused on their own balance sheet in the traditional business of banking - the rate environment would have had exactly the same effect. It already has had this effect.

In addition to the $620 billion in losses on securities, there exist staggering losses in the loan books of every bank that wrote fixed-rate loans from 2009 through 2021. Most people sensibly don't care about any of this and only care when a financial product core to their lives - bank deposits - suddenly and unexpectedly ceases to function.

Understanding Bank Deposits and Maturity Transformation

Bank deposits are much more complicated products than they're believed to be. When banks fail, the most important societal impact is that deposits, which are money no less than physical script (and in many ways more real), suddenly have an unanticipated risk of not being money.

What's the connection between deposits, bank runs, and the value of 10-year bonds in conditions of rising interest rates? You pay an explicit bill to most businesses which provide you valuable services. You get deposits for "free" (asterisk). The tellers, lawyers, engineers, regulators, insurance companies, and equity providers who collectively must labor diligently to give you deposits still need to get paid. They get paid largely by harvesting the option value from depositors as a class and creating something new out of it.

Banks engage in maturity transformation by borrowing short and lending long. Deposits are short-term liabilities of the bank - while time-locked deposits exist, broadly users can ask for them back on demand. Most assets of a bank (the loans or securities portfolio) have much longer duration.

Society depends on this mismatch existing. It must exist somewhere. The alternative is a much poorer and riskier world, which includes dystopian instruments so obviously bad you'd have to invent names for them. Take an "exploding mortgage," the only way to finance homes in a dystopian alternate universe. It's like the mortgages you're familiar with, except it's callable on demand by the bank. If you get the call and can't repay the mortgage by the close of the day, you lose your house. What did you do wrong to make the mortgage explode? Literally nothing. Exploding mortgages just explode sometimes. It keeps you on your toes.

Exploding mortgages don't exist and can't exist in our universe. But it's important that from a bank's perspective, the dominant way people bank creates that asymmetry - that mismatch. We expect banks to manage this risk, and we expect society to tolerate it (and sometimes cover the bill for it) because exploding mortgages are worse than this risk.

We have moved some of this mismatch out of the banking system by, for example, securitizing mortgages and selling them to pension funds, which can match them against natural liabilities. A pension fund calculates its natural liabilities using actuarial tables of when pensioners will retire and require their payouts. The banking system still holds a lot of duration mismatch risk. It likely always will.

Liquidity and Bank Failures

This is, like all other risks to banks, something which is managed and regulated. Sometimes management screws up or prioritizes their bonuses over prudential risk mitigation. Sometimes regulators are (feel free to choose your phrasing) asleep at the switch or not sufficiently empowered.

Let me quote from the FDIC speech from February 2023. While the FDIC obviously must moderate their public comments, this is the payload:

Unrealized losses on available-for-sale and held-to-maturity securities totaled $620 billion in the fourth quarter, down $69.5 billion from the prior quarter, due in part to lower mortgage rates. The combination of high level of longer-term asset maturities and a moderate decline in total deposits underscores the risk that these unrealized losses could become actual losses should banks need to sell securities to meet liquidity needs.

This is very measured language. Equally true language: About a quarter of all the equity in the banking sector has been vaporized by one line item. I was surprised to learn this. The sacred duty of equity is to protect depositors from losses. After it is zeroed, the losses must come from somewhere. We don't celebrate equity getting vaporized, except insofar as sacrifice of oneself in satisfaction of a duty to others is generally praiseworthy. But we certainly want to be aware that it happened.

The world is belatedly realizing that this did actually happen - past tense. The realization crept in around the edges with, for example, Byrne Hobart on February 23, 2023, noting that one of the US's largest banks was recently technically insolvent, but almost certainly in a survivable way. And to be fair, a few short funds and the Financial Times had come to this realization a bit before Byrne. Then, a few weeks later, the entire financial system almost simultaneously discovered how much they doubted precisely one half of his thesis.

Regulatory Oversight and Bank Failures

I submit to you that the regulators probably did not understand a few weeks ago that this situation was factually as concerning as it is. I submit to you that they probably did not understand what was happening in the exact week that this was happening.

Don't read this as a statement about competence or lack thereof. Just read it as a factual claim about the constitution of the Problem Bank List (PBL). The PBL is a figurative state secret, specifically to prevent inclusion on it from causing a run on the bank if it were to become common knowledge.

At least one bank which failed last week was not a problem bank three weeks ago. Reader, that should not ever happen. How do you know this, if the PBL is a state secret? Because federal regulators report the aggregate total of all assets of all banks on the list, and that publicly available data plus math a fourth-grader can do in their head suffices to prove this claim.

[Patrick notes: The FDIC routinely cites the aggregate total assets (and count of banks) on the PBL in their quarterly reports. For example, the Q3 2024 (released in December) report says:

The number of banks on the Problem Bank List, which encompasses banks that have a CAMELS composite rating of “4” or “5,” increased by two banks this quarter to 68 banks. The number of problem banks was within the normal range for non-crisis periods of 1 to 2 percent of all banks. Total assets held by problem banks increased $4 billion to $87 billion during the quarter.

And thus you can infer that e.g. Satander must not be on the PBL, because its assets are larger than the total assets of all banks on the PBL.

A similar exercise, conducted in March 2023, would have conclusively demonstrated that neither SVB nor First Republic was on the PBL.]

Finance is an industry with many smart people in it. The same goes for regulatory agencies. You're welcome to guess how many of them asked whether all of the banks which failed this week were on the Problem Bank List, or whether we had an unknown unknown prior to reading this paragraph.

Patrick comments: As an aside, many of us have a great deal of trust in the Efficient Markets Hypothesis, and nowhere is our degree of trust higher than for publicly traded U.S. equities. We should treat this failure to price in the risk of bank insolvency - approximately the most well-understood failure case known to capitalism - prior to this week in March as yet another empirical knock against the Efficient Markets Hypothesis.

Back to the essay: The same problems exist at banks that are not on the Problem Bank List. I would normally hedge that sentence with something like "likely." But the market has woken up and is now aggressively repricing risk and publishing findings. Those findings are deeply concerning, and for social reasons, I must direct you to the financial media of your choice to read them.

Patrick comments: Why these "social reasons"? Well, if you remember back to March 2023, people in the media were confidently claiming that shadowy tech elites, spurred on by venture capitalists, were intentionally killing banks to profit from shorting them.

[Patrick notes: This quixotic point of view was not confined to the media. As I’ve remarked in other situations: if banks simply start dropping like flies, that suggests that bank regulators are bad at their jobs. If, on the other hand, banks are being assassinated by shadowy conspiracies, then banking regulators are innocent. Accordingly, the government’s first instinct tends to be Oh Goodness, Are We Again Victims Of A Conspiracy By Nobody In This Administration? Once the professionals get around to writing the post-mortems that point of view gets quietly defenestrated, but nobody calls the WSJ to correct the record and say that e.g. the Secretary of the Treasury was slightly undisciplined with regards to past comments.]

That's a crazy theory, conclusively disproved by the experience of the intervening two years and by data showing that approximately 22 banks went through percussively explosive bank runs in the immediate wake of the first issues. But the media environment then was what it was, and I have a responsibility to both myself and many people dear to me to not get quoted in high-status journals as attempting to kill a bank by saying bad things about it.)

Back to the essay.

Recent History and Future Outlook

We went multiple years without a bank failure of any size in the United States. We then had three in a week, including one that by some measures was larger than any during the last financial crisis. After the March 2023 failures, First Republic went under great stress. An abortive rescue mission failed, and they eventually went under as of May 1st, 2023. We had two more smaller bank failures in 2023, and three since then - much less than the number of banks that could have failed or that actually experienced runs. So to a degree, the system, after waking up to the problem, actually worked. Yet this is more bank failures than we had in 2021-2022 combined.

Liquidity problems are the proximate cause of bank failures. The reason for relative sanguinity about unrealized losses in the banking sector (denominated in the hundreds of billions to low single-digit trillions of dollars) is that banks don't need to pay out all deposits simultaneously. Functionally, no bank anywhere could do that.

The theoretical exception, considered undesirable as a matter of public policy, is the so-called "narrow bank" - a commercial bank front-end to the Federal Reserve where all assets are just funds held at the Federal Reserve or equally impossible-to-fail assets like Treasuries. The bank would only allow customers to use payment methods backed by these narrow assets.

Patrick comments: Why don't we want narrow banks to exist? There are various reasons detailed in public position papers by regulators [Patrick notes: actually, less public comment about this than I expected, when looking late at night for a citation link], but it basically comes down to: 1) regulators don't buy advocates' arguments that narrow banks would solve existing problems, and 2) narrow banks would tend to cast doubt on the relative safety of other banks. We really don't like anything that casts doubt on the safety of the banking sector as a whole, so we just ban the concept entirely.

Understanding Bank Assets

Banks designate certain assets on their books as "available for sale" (AFS) - those they might sell to raise liquidity - and "held to maturity" (HTM). Losses in the AFS portfolio are relatively noisy because they immediately affect the income statement. They're reported quarterly and are extremely salient for all stakeholders. Losses in HTM securities are basically fine until they aren't.

This isn't entirely because management prefers to keep its head in the sand. Banks are institutions designed to exist over timelines longer than interest rate cycles. This implies certain assets will always be underwater, and certain assets will always be worth more than we paid for them. To the extent that the bank is simply holding the asset to collect income from it, this all comes out in the wash. The day-to-day movements are, in normal times, a distraction, relegated to a footnote.

We do not expect the footnote to swallow the bank, and that is an important update to our model of the world. We do not expect it to swallow multiple banks. We do not expect to not have a high-quality estimate for how many banks it will swallow in the next two weeks.

The three bank runs which already happened had idiosyncratic causes. But "if accounted for accurately, the bank is insolvent" is the sort of thing which, if stipulated to, might generate bank runs in the near future.

There was a policy response, which much commentary has assumed is primarily about the banks which no longer exist and the satisfaction of their depositors. That policy response is actually much more about banks in danger which might yet be saved - trying to forestall a banking crisis. The losses banks have taken on their assets are real. They already happened. They are survivable if those banks remain liquid.

[Patrick notes: It was a bit crazymaking to me, back in 2023, how many informed commentators believed that the decision to backstop SVB was simply a giveaway to Silicon Valley elites. Again, 22 bank runs in a universe of more than a thousand banks that were wobbling.]

The Federal Reserve, Department of Treasury, and Federal Deposit Insurance Corporation released a joint statement over the weekend to adjust people's expectations regarding banks that still exist. The key element of the response is a temporary extension of credit to banks, collateralized by high-quality assets at their par value rather than at their market value.

This is called the Bank Term Funding Program (BTFP). The hope is that a bank facing liquidity pressure could tap this credit program in addition to existing credit programs and sources of liquidity, thereby avoiding a downward spiral of selling assets, realizing losses, pushing asset prices down, spooking markets and depositors, and repeating at a very high cycle rate until the bank doesn't exist.

We recently went through that cycle faster than we thought possible with regards to a bank which responsible people considered very safe. According to the official record, one of the institutions went from financially healthy one day to insolvent the next. I believe that narrative to be face-saving, but it is what the system is currently messaging as the truth.

[Patrick notes: The official record which I was obliquely referring to is from the Commissioner of Financial Protection and Innovation in California. Under Findings of Fact, it reads:

Despite the bank being in sound financial condition prior to March 9, 2023, investors and depositors reacted by initiating withdrawals of $42 billion in deposits from the Bank on March 9, 2023, causing a run on the Bank.

Subsequent after-action reports by other regulators, such as e.g. the Federal Reserve, made statements which, how should I put this delicately, acknowledge reality. Even those statements are often couched to throw SVB under the bus and minimize potential deficiencies in regulation, but if you parse them closely, there is some degree of awareness. For example, see Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank:

Silicon Valley Bank (SVB) failed because of a textbook case of mismanagement by the bank. Its senior leadership failed to manage basic interest rate and liquidity risk. Its board of directors failed to oversee senior leadership and hold them accountable. And Federal Reserve supervisors failed to take forceful enough action, as detailed in the report.

]

Program Timeline and Moral Hazard

The BTFP is a temporary program - banks can only tap this liquidity for about a year. In the ordinary course, bank runs don't last for a year. They either cause an institution to fail very quickly, or they peter out.

But there's another reason this is time-bounded: moral hazard, on behalf of both banks and their customers. Moral hazard in insurance is when the existence of insurance makes it incentive-compatible for you to be imprudent in your own risk-taking, expecting someone else to bear the consequences. Banking regulators want banks to take the strong medicine solution to the problem.

Limited Options

If banks have experienced hundreds of billions to single-digit trillions of dollars in losses, realized or not, they have a very limited set of options:

- Hoping for a miracle

- Experiencing a sudden dramatic shift downwards in interest rates, which would cause them windfall gains for exactly the reason they experienced windfall losses

- Grinding out many years of profits in the ordinary business of banking to fill the hole

But the thing which is actually within their immediate ability and control is simple and painful: The sacred duty of equity is to take losses before depositors do. Equity has taken losses. Depositors must be shielded. Equity must be raised to take the losses again.

[Patrick notes: SVB attempted to raise equity and failed to do so, which (in the context of the run) was the final straw. Similarly, First Republic also spent March through May attempting to do capital raises, and could not find a price; its equity was worthless.

There was a consortium which attempted to backstop First Republic by depositing ~$30 billion into CDs, to shore up their liquidity. One assumes this was stagemanaged by federal regulators who gave the other banks both an guarantee that their deposits would be protected and signaled that regulators were strongly in favor of pro-social gestures given the environment.

But is it likely that any regulator ordered the largest banks in the world to deposit money in an ailing regional bank? Of course not; this is America. We’re not communists.]

Market Dynamics and Equity

Equity, of course, has a choice in a free market system as to which risks it wants to take. It flowed into banks in good times at prices banks were reasonably happy with. They now need to raise capital in what is no longer a good time at prices banks and existing equity holders won't be happy with, because the new marginal equity appreciates the risk environment it's entering more than the equity raised earlier.

This is the short explanation for why bank stocks are getting hammered right now. A share is a one-over-sum denominator claim on the equity of a bank. Sophisticated people are realizing that the numerator is lower than they expect, and the denominator is shortly to be larger, and potentially much larger than they expect. Existing shares are perforce worth less than they were before we came to this realization. Banks will need to go to the market to sell new shares at these less favorable prices.

Market Efficiency Questions

This serves as another knock against the strong-form efficient markets hypothesis. None of these dynamics are particularly complicated by the standards of finance. The core facts weren't secrets - they were exhaustively disclosed on a quarterly basis. Charts were made. Anyone could have made a killing if they put two and two together even a week ago. A killing was, mostly, not made.

(Parenthetical note: killings perhaps remain available as of this writing, if that is your thing.)

The First Republic Case Study

Patrick comments:

At the time, I very much did not want to name the bank that was most obviously wobbling, even though it was publicly reported as most obviously wobbling. That was First Republic. In the intervening time, we learned that First Republic was not merely wobbling but was actually in a situation which was not solvable despite much effort from many people to save the bank.

Let me share a quick history of First Republic share prices because, again, markets aren't necessarily efficient:

- March 1st, 2023: Trading at about $120 (a week before things went south)

- March 10th (Friday): Closed at $82

- March 13th (Monday after Signature Bank's seizure): Closed at $31

- March 14th (when I published my essay): Bounced up to $40

If you had hypothetically read the essay and decided First Republic wasn't savable despite extraordinary efforts being messaged, you could have shorted it from $40 straight to zero. You could have shorted it from $120 to $40 taking much less risk if you had simply put two and two together a few weeks earlier based on, among other things, reading Byrne Hobart's essay and taking it to its logical conclusion.

But logical conclusions weren't common knowledge until they suddenly were, and banks started dropping by tens of percent a day. Is this totally a knock on the efficient market hypothesis? No - there were 22 banks under a run at this point. We didn't know that fact until much later. But many bank stocks were being hammered by investors (and "speculators" is perhaps not the right word) as information about banks' large structural balance sheet problems started to flow into the market at vastly accelerated rates.

Many bank stocks got hit very hard with very quick runs, exceeding five standard deviations of standard banking practice at 22 institutions. Of those 22 institutions, only about three that survived past the date of this essay failed, but calculating whether a short would have made money betting on this thesis is slightly more complicated than that.

Patrick notes: One of the most obvious trades, and goodness was there some interest in it, was simply shorting an index of regional bank stocks. For example, and for purposes of identification only, IAT is an ETF which tracks an iShares index of those banks. IAT was extremely heavily shorted in March 2023, to the point where (IIRC) it was on the “hard to borrow list in some places. This is extremely unusual for index fund ETFs.

Trading volumes more than 5Xed the week of the 13th compared to the week previous, as capitalism started to digest what it now knew, and spool out implications. (You’ll note something of a recovery in the intervening two years, as the market increasingly believes that banks which have survived to this point will likely survive.)

The Evolution of Deposit Insurance

Bank deposits in the U.S. are insured up to $250,000 per depositor per account type per institution. The exact definition of account type is a wonky detail - just assume it's $250,000 historically per depositor/institution pair, and you'll save some brain cells for the more important issues.

Patrick comments: This wonky detail involves things like how you personally could have $250,000 of coverage for deposit insurance, but if you hold a joint account perhaps under some sort of trust structure, you can double dip. Don't try to use that wonky detail to develop a strategy unless this is professionally your job. The much easier way is to just go to someone who is selling you the ability to put your deposits at multiple banks simultaneously. [Patrick notes: This is described below, so I’ll elide the mechanics here.]

Back to the essay: By special and extraordinary action, the FDIC announced that two recent bank failures will backstop all deposits, not just insured deposits. Much commentary has focused on the decision to create winners out of losers - these depositors at these two institutions. This is an effect of the policy, but it's neither the intent nor the rationale.

Behind the Scenes of the Crisis

Patrick comments: I will try to avoid sounding borderline smug when reading the following, for reasons which will soon become clear.

The essay: Let me speculate about some things which may have happened this weekend, with arbitrarily high confidence.

Over the weekend, regulators made some calls and asked regional banks what deposit outflows looked like Friday and how many wires were queued up for execution Monday morning. This was complicated by some banks finding it surprisingly difficult to add numbers quickly. The core banking system puts queued wire requests in a different part of the system than Friday's outflows. They had a report of Friday's outflows, but it only gets crunched by an ETL job that finishes halfway through Saturday. And Cindy, who understands all this, was on vacation.

Patrick comments: This prediction turned out to be almost exactly what happened with Signature Bank. Their operational competence issues, specifically their inability to give regulators an up-to-date count of Monday morning's queued wires plus a worst-case scenario projection, led to regulators losing trust in their basic banking capabilities. This was cited as one reason why they declared the bank failed on Sunday and pursued a resolution.

[Patrick notes: See the New York State Department of Financial Services Internal Review of the Supervision and Closure of Signature Bank, which I comment extensively on in the debanking essay.]

Did I specifically know this about Signature prior to writing this? No, but there exists something like a general factor of infrastructure, meaning that this field (and I'm gesturing broadly to any number of interconnected fields) is not unknowable. You can have good intuitions based on things you've observed in other instances of analogous subfields.

ETL (Extract, Transform, Load) is a technologist term for the data pipeline that moves something from a source of truth, such as a database, into something more comprehensible by decision makers, such as a report. So while you might have one or more sources of truth at your financial institution about pending wire transfers, the ability to read that number to a regulator depends on either an analyst typing queries very fast into the database, or more likely, some sort of ETL pipeline that collates information from various subsystems and generates reports with some latency.

[Patrick notes: One very non-obvious observation about banks during the crisis: one reason why people were so focused on “mobile apps” was that the mobile app people have, for technological/structural reasons, the ability to get up-to-the-minute counts of events within mobile apps, and “the money people” have higher latency. And thus the mobile app people were perceived as being the ones causing the crisis, because they understood that outgoing wires were spiking hours before the money people did.

This isn’t just “wet streets create rain”, this is “people photographing wet streets create rain, because clearly writing ‘the street is wet’ takes more effort and is clearly downstream of the photograph.”]

The Regulatory Response

Regulators then heard the numbers, did some modeling in Excel, and went into wartime execution mode. Regulators haven't declared this war, because it's a war on the public's perception of reality, and to declare war is to surrender.

The $620 billion in losses on securities, and the concomitant loss on loans, isn't distributed evenly across the U.S. banking sector. Every institution thanking its risk managers for having a below-average amount implies that some other institution has an above-average amount. Some institutions whose names aren't yet in headlines but maybe very shortly indeed are under acute stress.

We're beginning to understand a mechanism by which a handful of institutions fell off a precipice because we understand the edge of that precipice to be eroding as we believe current interest rates will go up again. This belief is shifting rapidly - the rapid decline in two-year Treasury yields is a sign that markets are adjusting expectations and beginning to doubt the forecast future sharp hikes.

Financial institutions are adjusting to the new reality rapidly. Over the weekend, like every other customer of a particular bank, I got an email from the CEO explaining that they had ample liquidity but had just secured a few tens of billions of dollars of additional liquidity - prudent risk management, no problems here, all services are up as ever.

Patrick comments: (As an aside, that bank was First Republic, and the CEO wrote a measured email to depositors who loved that institution. This is factually a communication strategy often adopted by banks in crisis. Of course, the crisis management at First Republic and attempts to resolve it were ultimately unsuccessful.)

The essay continues: Securing more liquidity may be prudent, and announcing it may be prudent, but this is not an email you send to all customers in good times. Banks typically take communications advice from the Lannisters: Anyone who needs to say they have adequate liquidity does not have adequate liquidity. History is replete with examples. Bank CEOs know this. They know their sophisticated customers know this. And yet, that email was written, reviewed by management and crisis communications and counsel, and then sent.

The Evolution of Deposit Insurance

Deposit insurance has some legacy issues. It's an important piece of social technology - so successful that some believe it is the primary reason deposits are safe. It is, of course, the backstop to the primary things that make deposits safe:

- The ordinary risk management of banks

- A complex and mostly effective regulatory regime

- $2.2 trillion of private capital that's signed up to be incinerated if there are faults in earlier controls

The Deposit Insurance Fund, by comparison, is about $130 billion, which you can compare to that $620 billion in losses number prior to thanking capital for its service to society.

Much like credit cards are legacy infrastructure, deposit insurance is also legacy infrastructure. It is designed to adjust the expectations of large numbers of relatively slow-acting and low-sophistication users by credibly dampening the pain to regular users of the banking system that banking stress threatens.

But the world deposit insurance now protects is different than the one it was developed in, and I think it may need to be updated. One much-remarked-upon change is that some banks have hyper-networked customer bases, and they can, through relatively independent action, tweet and WhatsApp themselves to withdrawing $42 billion in a day.

Professional Runs vs. Retail Runs

But deposit insurance is institutionally aware that some institutions have concentrated deposits, and lots of deposits are controlled by sophisticated actors. We had capital-intensive businesses with chain-smoking professionals who preferred their businesses to survive a bank run during all the relevant crises. The architects of deposit insurance knew these people exist, and that they were a primary vector for runs historically. This problem is planned for! It was not created by Twitter.

Patrick comments: The paper from the Federal Reserve Bank of New York conclusively demonstrates that retail runs were not a contributor during any of these runs or bank failures. The primary runs were through financial professionals moving brokered deposits.

This is one of the most salient things to understand about Signature Bank - they weren't killed by the run on crypto assets. They were killed by New York commercial real estate operators and deposit brokers mutually deciding to move their operating funds and brokered deposits away from Signature.

In the case of the brokers, they were often moving their "time-locked" deposits. What they were saying, effectively, in moving a time-locked deposit is: "If this is a certificate of deposit, there is some fee that I have to pay to move this $50 million out of the bank today. I'm willing to pay that fee because I don't think your bank will be around on Monday."

Indeed, those sophisticated risk managers rewriting the credit risk of their counterparties were correct in their analysis.

[Patrick notes: Quoting New York’s after-action again:

Due to its focus on cultivating commercial clients, Signature constantly maintained a high percentage of uninsured deposits. As of year-end 2018, Signature’s uninsured deposits totaled $30 billion, representing 63 percent of the Bank’s total assets. By December 31, 2021, uninsured deposits had more than tripled, totaling approximately $98 billion, representing 82 percent of Signature’s total assets. Signature’s reliance on uninsured deposits posed a risk that the Bank had to manage carefully to ensure adequate liquidity while maintaining a safe and sound business. The essential risk is that uninsured depositors may quickly withdraw their deposits if there is any risk that their bank may fail, because their uninsured status means they may not fully recover their funds in the event of a failure.

]

Modern Banking Challenges

Let's talk about the problem deposit insurance doesn't institutionally prepare us for. The entire edifice of deposit insurance rests on the assumption that the primary harm from bank failure, at least the one worthy of societal attention, falls first on direct depositors of the bank and secondarily on spillover stress to the rest of the system. This is a reasonable model, and like all models, it is wrong but useful.

Consider the case of Rippling, a startup I have no affiliation with. Rippling has a complicated business, with one portion being a payroll provider. Payroll providers as a type of business are much older than iPhones but effectively younger than many policy measures designed to mitigate banking crises.

When Rippling's bank recently went under, there was substantial risk that paychecks would not arrive for employees of Rippling's customers. Rippling wrote a press release titled "Rippling calls on the FDIC to release payments due to hundreds of thousands of everyday Americans."

Prior to the FDIC's decision to entirely back the depositors of the failed bank, the amount of coverage the deposit insurance scheme provided depositors was $250,000, and the amount it afforded someone receiving a paycheck drawn on the dead bank was $0.00. This is not a palatable result for society - not politically, not economically, not as a matter of policy, not as a matter of ethics.

Every regulator sees the world through a lens painstakingly crafted over decades. The FDIC institutionally looks at this fact pattern and sees a single depositor over the insured deposit limit. It does not see 300,000 bounced paychecks.

The Evolution of Banking Infrastructure

Payroll providers are just the tip of the iceberg for novel innovations in financial services over the last few decades. There exist many other things which society depends upon that map very poorly to the insured account abstraction. This likely magnifies the aggregate impact of bank failures and makes some of our institutional intuitions about their blast radius wrong in important ways.

What would happen if my bank were to go into receivership this weekend? Historically, the dominant answer is that it's sold and you have a new bank on Monday with functionally nothing else changing. The system has worked very well. We've gone years since the last bank failure. Most failures are small, most are entirely resolved by the following Monday, and even deposits over the limits at failed banks have rarely taken losses over the last few decades. When they have, those losses have been minuscule.

The system recently looked at the combination of published rules, availability of a transaction over the weekend, degree of surprise, preparedness of suitors, and it blinked because of what it could have actually delivered on Monday: The full satisfaction of insured deposits, and perhaps 50 cents on the dollar of uninsured deposits, with a few months of uncertainty as to the timing and level of satisfaction for the remainder. Actual losses would have probably been zero or a few cents on the dollar, eventually. Probably.

That resolution is much worse than the one the system typically obtains and would have affected many more people than is typical. This may be, if not the new normal, a new concerning potential recurring pattern during uncertain times.

The Reality of Modern Banking Structures

People may have a mental model that a bank keeps a list of all its customers and can therefore quickly calculate who is insured and to what degree, so it can pass this list to the FDIC for Monday payouts. This is a useful mental model for first approximations but does not actually describe the world you live in.

FDIC insurance insures the actual owners of accounts and not entities those accounts are titled to. One important type is the "for benefit of" (FBO) account, where someone might hold money in trust for someone else in their own name. FBOs aren't newfangled things dreamt up in Silicon Valley - trusts as an institution date back to the Middle Ages.

Decades ago, the dominant mental image for FBO accounts might have been Lawyer Larry holding a settlement on behalf of Client Carla. The FDIC insures Carla, not Larry, even if Larry has 50 Carlas commingled in a single account and the bank only knows them as names available upon request.

This might surprise people who think banks need to know their customers. The bank customarily adheres to its written policy about KYC for FBOs. Their regulator is okay with this policy. All of this is the normal business of banking and entirely uncontroversial. To make Carla whole, the FDIC has to learn Carla exists first, which implies a process that cannot conclude by next Monday.

The Fintech Challenge

You might think this is an edge case - lawyers and FBO accounts must be a tiny percentage of all deposits, and while this would be greatly inconvenient for Carla, presumably if she's still banking through her lawyer in 2023, she's rich and sophisticated.

Let's talk about fintech. Many fintech products have an account structure that looks like this: A financial technology company has one or several banking relationships. It has many customers - enterprises who use it for payment services or custodying money. Those services aren't formally bank accounts, but they perform a lot of "feels kind of bankish if you squint at it" functions for people who rely on them to feed their families.

The actual banking services are provided by banks who are disclosed prominently on the bottom of the page and in the terms and conditions. Each enterprise has their own book of users, who might number in the hundreds of thousands or millions, in a single FBO account at the bank, titled in the name of the enterprise or the fintech.

The true owners of the funds are known to the bank to be available in the ledgers of the fintech, but the bank may have sharply limited understanding of them in real time. Is this structure robust against the failure of a bank handled other than cleanly, such that come Monday, those users receive the insurance protection afforded them by law?

Mechanically, can that actually be done? Is our society prepared to figure that out over a weekend? During this past weekend, that sketch I wrote about banks being confuddled by addition for a few hours almost certainly happened - and we now positively know that it did.

There are a sharply finite number of hours between Friday and Monday, and we cannot conveniently extend them to cover multi-party discussions about how to get a core system to import a CSV dumped by a debleaguered data scientist from Jupyter based on a hopefully up-to-date MongoDB snapshot, so it can be provided to the FDIC agents on site.

[Patrick notes: As mentioned in a few paragraphs, this is keenly relevant not merely in the case of failure of banks, but also in failures of intermediary firms, though the resolution pathway for them is very different.

Of course, I did not in March 2023 have access to the report of the bankruptcy trustee for Synapse filed in 2024. I am unlikely to be able to comment further, partly because of social reasons, but echoing a previous observation: one can see around corners if one devotes effort into studying spiritually analogous complex systems.]

The Social Impact of Bank Failures

I am very frustrated by political arguments about desert, which start with an enemy's list and celebrate when the enemies suffer misfortune for their sins, like using the banking system. The majority of those uninsured deposits were $1 billion kept at SVB securing the USDC stablecoin treasury, a product of a consortium involving Coinbase and Circle.

Patrick comments: I'm a bit of a crypto skeptic but think that nobody needs to be bankrupted just because they chose to use the banking system. That should be a reliable piece of societal infrastructure.

Most enemies lists don't include taxi drivers, florists, teachers, plumbers, etc. Literally every strata of society is exposed to products which bank for them in complicated ways. These people will be hurt by bank failures.

We as a society do not accept this, which is why they are protected if they bank directly with a financial institution, and why we promise they are protected if their money is in a more complicated account structure.

The Future of Banking Infrastructure

Many people might feel surprise that structures like this exist and are deployed pervasively. Was that allowed? Where were the regulators? Yes, it was allowed. The regulators were in the usual places.

Interestingly, this has not been the dominant worry about the adequacy of deposit insurance in the fintech industry. The dominant worry among clueful people on this narrow and wonky topic has been that deposit insurance would not protect some people exposed to structures where the bank survived but the fintech did not.

[Patrick notes: We, unfortunately, now have existence proofs of this risk. See, for example, the collapse of Synapse, about which you can read much more elsewhere.]

The good news is that the problem we're immediately faced with is the sort of thing that deposit insurance actually insures against - the failure of financial institutions. The hypothetical losses would be covered. The bad news is that banks are failing! More may fail, potentially including some banks with customers that have business models younger than "It's a Wonderful Life" from 1946.

Practical Advice for Banking System Users

What should users of the banking system do? While I suggest going to someone who actually has a professional duty of care to you, here are some general observations:

- The banking system is more resilient than appreciated, even under conditions of immense stress. From the perspective of the typical consumer, you can probably blithely ignore that this is happening.

- To the extent you want to take low-cost actions you're unlikely to regret:

- Have at least one backup financial institution

- Remember that opening bank accounts rounds to free

- Consider putting enough in a backup account to get through a weekend or payroll cycle

- Have credit available at diverse institutions

This has the added benefit of helping if the issue is total computer failure rather than financial catastrophe. Speaking of which, total computer failure definitely happened in 2024 due to the CrowdStrike bug - a correlated failure that hit multiple financial institutions simultaneously due to the monoculture among security providers for banks.

Business Considerations

For businesses, the considerations are more complicated. Many believe that businesses should have a treasury department focused solely on liquidity and risk management. That sounds great in theory, but in reality, you typically hire a treasury department at a few hundred employees after your bank account is above FDIC coverage limits. Deposit insurance was designed for a world with sharply different employment patterns.

Many banks and technology firms have various automated treasury management solutions that can do some of the work of a treasury department at a tiny fraction of the cost. It seems popular now to shame businesses and suggest they need to manage their bank's counterparty risk. This is actually advocacy for the most sophisticated financial firms to have a new high-margin revenue stream renting solutions to businesses too large to benefit from deposit insurance but too small to hire a treasury department.

The basic offering is establishing relationships with multiple banks in parallel, automating money movement between them so you can treat your money as one logical pile while keeping a maximum of $250,000 in each institution. This effectively multiplies your deposit insurance coverage. There are thousands of banks, and these providers are tireless in finding partners.

Final Thoughts

The banking system is well regulated, resilient, and strong. Most U.S. institutions are comfortably okay at the moment, though some may not be. Failures, particularly surprising ones, in heavily interconnected core infrastructure have a worrisome tendency to cascade.

This is not the end of the world, but in the last five days, we've had a material and negative update on our understanding of the state of the world. It has surprised many people at many different institutional vantage points - people you'd expect not to be surprised by this exact issue.

Looking Back Two Years Later

This essay holds up reasonably well two years later.

But one thing that doesn't hold up is the protestations that the bank runs were uniquely generated by social media. Consider these quotes:

- "SVB is the first social media bank run in history. This crisis will change the banking industry forever." - headline, Business Insider

- "The first social media internet bank run in history." - Senator Mark Warner

- "No matter how strong capital and liquidity supervision are, if a bank has an overwhelming run that's spurred by social media or whatever so that it's seeing deposits flee at that pace, a bank can be put in danger of failing." - Janet Yellen, Treasury Secretary

[Patrick notes: Senator Warner’s further comments included

I’ve been supportive of the venture capital community — I was a venture capitalist before — but I think there were some bad actors in the VC community who literally started to spur this run by virtually crying fire in a crowded theater in terms of rushing all these deposits out.]

Social media did not do this - there was no retail run. [Patrick notes: Anywhere, according to the Federal Reserve paper. The thing which happened was accurate, high-velocity risk management by professional managers of money tasked with risk management.]

These people did not understand the thing we pay them to understand. Was that fact available to them in the same week? Very plausibly yes.

The unfortunate bit about our intuitions regarding democratic governance is that we generally expect the government to tell us the truth as it understands it. We have limited carve-outs - during military operations, we don't live-tweet troop positions, and we don't exhaustively disclose intelligence gathering. But we don't generally treat statements about the banking industry as strategic communications - for example, lying if necessary to achieve other objectives.

I would say that the government routinely does strategic communications to protect the banking system's stability. That's a usual and useful thing for people interested in democratic governance to understand. (And that statement is totally in my personal capacity - you probably shouldn't expect to see me appointed as Treasury Secretary anytime soon.)

Thanks for tuning into this week's episode of Complex Systems. If you're interested in topics like this, check out Bits about Money. For comments, email me or find me as patio11 on Twitter. Ratings and reviews help new podcasts tremendously, both for SEO reasons and because they let me know what you like.